250711121524608~.jpg)

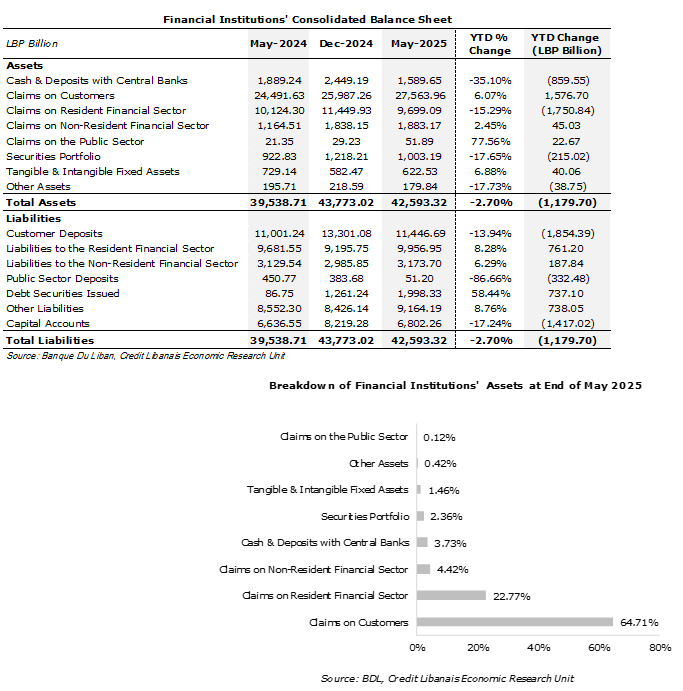

According to Banque Du Liban (BDL) statistics, the consolidated balance sheet of financial institutions operating in Lebanon narrowed by 2.70% (LBP 1,179.70 billion) in the first five months of 2025 to LBP 42,593.32 billion, down from LBP 43,773.02 billion at year-end 2024. This can be attributed to the 15.29% (LBP 1,750.84 billion) decrease in claims on the resident financial sector to LBP 9,699.09 billion, coupled with the 35.10% (LBP 859.55 billion) drop in cash & deposits with central banks to LBP 1,589.65 billion and the 17.65% (LBP 215.02 billion) decrease in the value of the securities portfolio to LBP 1,003.19 billion, which altogether outweighed the 6.07% (LBP 1,576.70 billion) increase in claims on customers to LBP 27,563.96 billion, the 2.45% (LBP 45.03 billion) rise in claims on the non-resident financial sector to LBP 1,883.17 billion, and the 6.88% (LBP 40.06 billion) increase in the value of fixed assets to LBP 622.53 billion, among others. It is worth noting that claims on customers and claims on the resident financial sector are the two largest asset categories on financial institutions’ balance sheet, accounting for 64.71% and 22.77% of total assets on a respective basis. On the liabilities side, customer deposits dropped by 13.94% (LBP 1,854.39 billion) YTD May 2025 to LBP 11,446.69 billion, with capital accounts decreasing by 17.24% (LBP 1,417.02 billion) to LBP 6,802.26 billion and public sector deposits plummeting by 86.66% (LBP 332.48 billion) to LBP 51.20 billion, totally eroding the 8.28% (LBP 761.20 billion) increase in liabilities to the resident financial sector to LBP 9,956.95 billion, the 8.76% (LBP 738.05 billion) rise in other liabilities to LBP 9,164.19 billion, and the 58.44% (LBP 737.10 billion) increase in the value of issued debt securities to LBP 1,998.33 billion only to name a few.

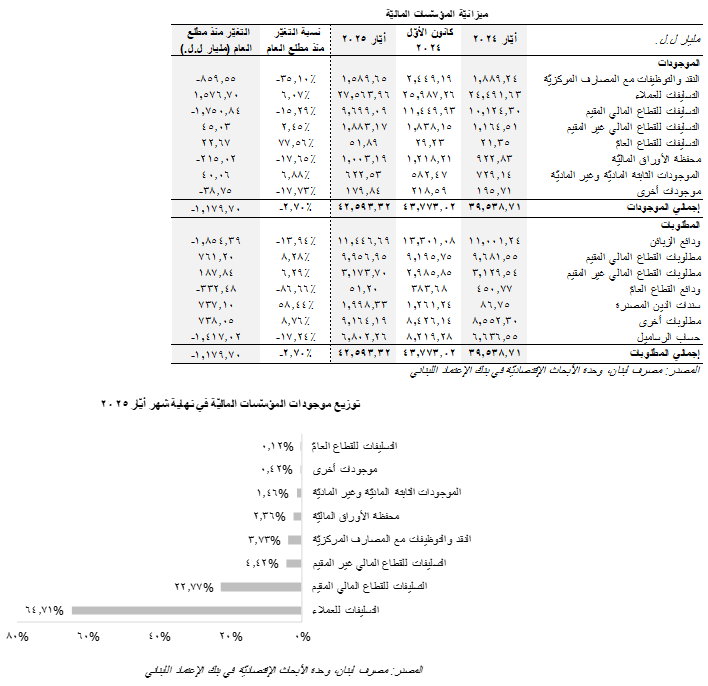

إستناداً إلى إحصاءات مصرف لبنان، إنخفضت الميزانيّة المجمَّعة للمؤسَّسات الماليّة العاملة في لبنان بنسبة 2.70% (1،179.70 مليار ل.ل.) في الأشهر الخمسة الأولى من العام 2025 إلى 42،593.32 مليار ل.ل.، من 43،773.02 مليار ل.ل. في نهاية العام 2024. يُنسَب هذا الإنخفاض بالأخصّ إلى تراجع التسليفات للقطاع المالي المقيم بنسبة 15.29% (1،750.84 مليار ل.ل.) إلى 9،699.09 مليار ل.ل.، ترافقاً مع إنخفاض رصيد النقد والتوظيفات مع المصارف المركزيّة بنسبة 35.10% (859.55 مليار ل.ل.) إلى 1،589.65 مليار ل.ل. وتدنّي قيمة محفظة الأوراق الماليّة بنسبة 17.65% (215.02 مليار ل.ل.) إلى 1،003.19 مليار ل.ل.، ما طغى على إرتفاع التسليفات للعملاء بنسبة 6.07% (1،576.70 مليار ل.ل.) إلى 27،563.96 مليار ل.ل. وزيادة التسليفات للقطاع المالي غير المقيم بنسبة 2.45% (45.03 مليار ل.ل.) إلى 1،883.17 مليار ل.ل. وإرتفاع قيمة الموجودات الثابتة بنسبة 6.88% (40.06 مليار ل.ل.) إلى 622.53 مليار ل.ل. للذكر لا للحصر. يجدر الذكر أنّ محفظة التسليفات إلى الزبائن والتسليفات للقطاع المالي المقيم هما أكبر مُكوِّنين لميزانيّة المؤسَّسات الماليّة، بحيث بلغت حصّتهما 64.71% و22.77% بالتتالي من مجموع الأصول المجمّعة مع نهاية شهر أيّار. أمّا على صعيد المطلوبات، فقد إنخفض رصيد ودائع الزبائن بنسبة 13.94% (1،854.39 مليار ل.ل.) حتّى شهر أيّار من العام الحالي إلى 11،446.69 مليار ل.ل. وتراجع رصيد حساب الرساميل بنسبة 17.24% (1،417.02 مليار ل.ل.) إلى 6،802.26 مليار ل.ل. كما وتدنّت ودائع القطاع العامّ بنسبة 86.66% (332.48 مليار ل.ل.) إلى 51.20 مليار ل.ل.، ما أطاح بزيادة مطلوبات القطاع المالي المقيم بنسبة 8.28% (761.20 مليار ل.ل.) إلى 9،956.95 مليار ل.ل. وإرتفاع قيمة المطلوبات الأخرى بنسبة 8.76% (738.05 مليار ل.ل.) إلى 9،164.19 مليار ل.ل. وزيادة قيمة سندات الدين المصدرة بنسبة 58.44% (737.10 مليار ل.ل.) إلى 1،998.33 مليار ل.ل.، للذكر لا الحصر.