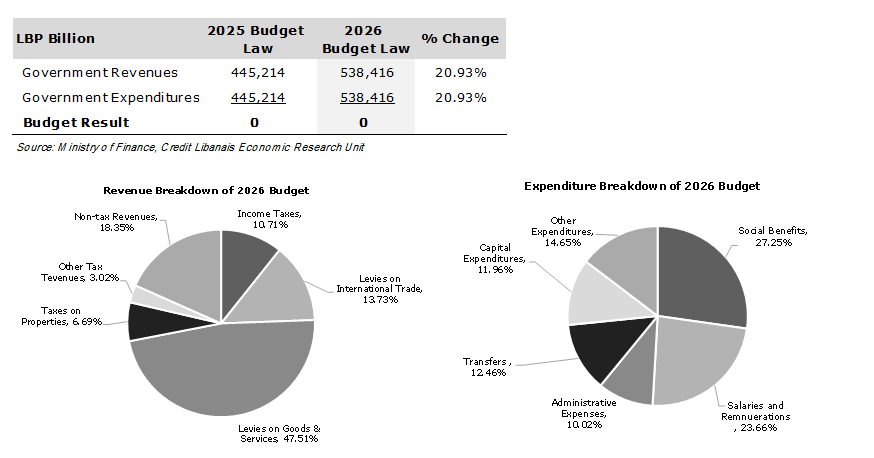

The Lebanese Parliament recently ratified a balanced budget law for the year 2026 targeting revenues and expenditures of LBP 538.42 trillion (around $6.01 billion) each, up by 20.93% from year 2025’s budget law figures of LBP 445.21 trillion (around $4.97 billion). It is worth noting that in accordance with the practice established in recent years, the 2026 budget law does not include an advance to Eléctricité du Liban (EDL) after the latter revised its tariffs to stand above production costs. The budget suggests a high contribution from tax revenues of LBP 439.61 trillion, representing 81.65% of total revenues, with non-tax revenues (LBP 98.80 trillion) expected to represent 18.35% of target revenues. Delving into details, levies on goods and services (LBP 255.79 trillion vs LBP 203.55 trillion in the 2025 budget law) are budgeted to be the major contributor (47.51%) to total revenues, with levies on international trade (LBP 73.91 trillion vs LBP 73.39 trillion in the 2025 budget law) and taxes on properties (LBP 36.01 trillion vs LBP 29.50 trillion in the 2025 budget law) accounting for 13.73% and 6.69% of total revenues respectively. It is worth noting, in this perspective, that non-tax revenues mainly represent revenues from state owned enterprises such as Casino du Liban, Lebanese ports, the Rafik Hariri Beirut International Airport and the telecom sector among others. The law raises several penalties by a factor of 25 times while also increasing the reporting obligations related to Ultimate Beneficial Ownership “UBO” (a step that can aid in combatting money laundering and adhering to international best practices), whereby concerned individuals must notify relevant tax authorities of any changes in UBO within one month (compared to two months previously) of the date of change, while simultaneously hiking the fees related to non-compliance with said requirements. The law also imposes fees on foreign trucks that cross the Lebanese territory for international transport purposes, except for trucks belonging to countries that exempt Lebanon from said fees according to bilateral trade agreements. The law increases the percentage fee allocated to sellers of fiscal stamps to 7% (from 5% previously) of the value of the stamp, in order to incentivize them to sell stamps at their nominal value, while also setting the minimum daily meal allowance for private sector employees at LBP 300,000. In addition, the law stipulates that the customs administration must levy a 1.5% charge on every import transaction, with the amount considered as an advance on the importer’s income tax. Always on the revenues front, several fees associated with transactions with the Directorate of General Security (including the fees related to residencies for those holding work permits) were increased. The law also levied a 17% “exceptional” tax on profits realized on Sayrafa transactions that exceeded $100,000. Finally, the law hiked the penalty imposed on tourism companies that organize foreign groups’ tours for each person under their responsibility who fails to depart to LBP 180 million (from LBP 3 million previously).

On the expenditures front, social benefits are expected to account for over one-quarter (27.25%) of total budgeted expenditures, followed by salaries & remunerations (23.66%) and transfers (12.46%; part of which is geared towards salaries and transfers to non-profit organizations). Other significant expenditure items include capital expenditures (11.96%) mainly in the form of governmental expropriations, and administrative expenses (10.02%).

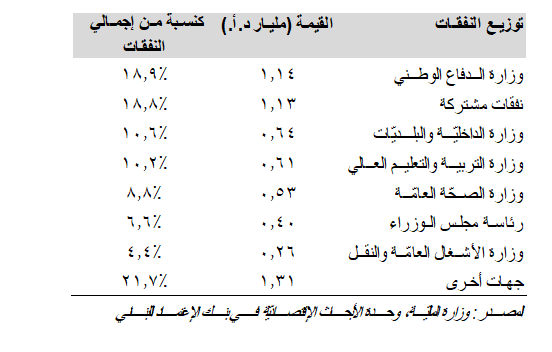

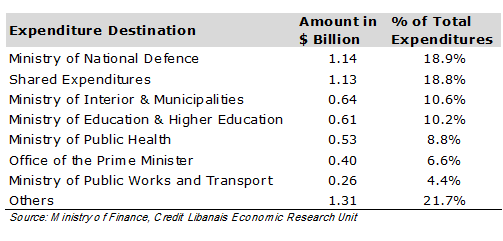

Furthermore, the largest portion of budgeted expenditures was allocated to the Ministry of National Defense ($1.14 billion; 18.9%), followed closely by shared expenditures ($1.13 billion, 18.8%), the Ministry of Interior and Municipalities ($0.64 billion, 10.6%) and the Ministry of Education and Higher Education ($0.61 billion, 10.2%) only to name a few. This is further reflected by the below table:

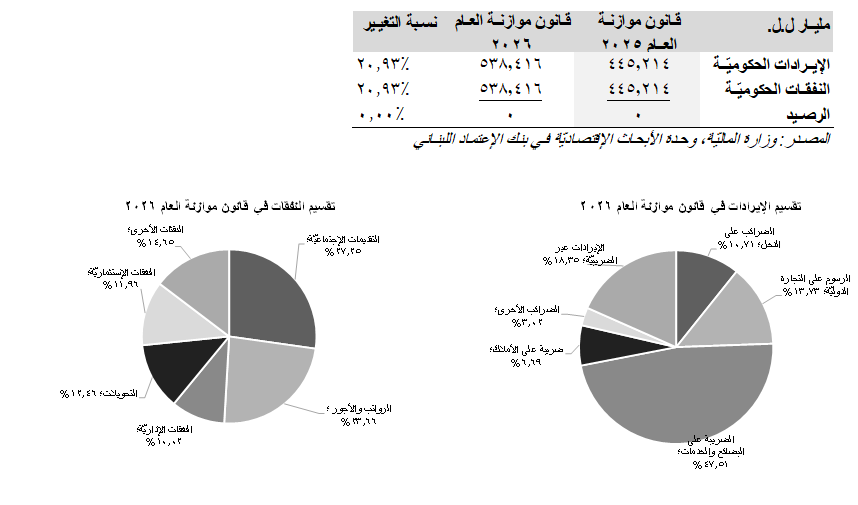

أقرّ مجلس النوّاب مؤخّراً قانون موازنة العام 2026 والذي يظهر توازن بين الإيرادات والنفقات الحكوميّة عند 538.42 تريليون ل.ل. (حوالي 6.01 مليار د.أ.) لكلٍّ منها أيّ بزيادة نسبتها 20.93% عن أرقام قانون موازنة العام 2025 البالغة 445.21 تريليون ل.ل. (حوالي 4.97 مليار د.أ.). ويجدر الذكر في هذا السياق بأنّ قانون الموازنة الحالي (وأسوةً بمشاريع قوانين الموازنة مؤخّراً) لا يلحظ سلفة لمصلحة مؤسّسة كهرباء لبنان وذلك بعد قيام هذه الأخيرة بتعديل تعرفتها لتفوق كلفة الإنتاج. وقد لحظ قانون الموازنة مساهمة كبيرة (81.65%) للإيرادات الضريبيّة لتصل إلى 439.61 تريليون ل.ل. فيما يتوقّع أن تشكّل الإيرادات غير الضريبيّة (98.80 تريليون ل.ل.) نسبة 18.35% من الإيرادات المستهدفة. بالتفاصيل، تتوقّع الموازنة أن تشكّل الضرائب على السلع والخدمات (255.79 تريليون ل.ل. مقابل 203.55 تريليون ل.ل. في قانون موازنة العام 2025) الحصّة الأكبر 47.51% من إجمالي الإيرادات الحكوميّة تليها الرسوم على التجارة الدوليّة (73.91 تريليون ل.ل. مقابل 73.39 تريليون ل.ل. في قانون موازنة العام 2025) بنسبة 13.73% من إجمالي الإيرادات والضرائب على الأملاك (36.01 تريليون ل.ل. مقابل 29.50 تريليون ل.ل. في قانون موازنة العام 2025) بنسبة 6.69% من إجمالي الإيرادات. ومن الجدير الذكر في هذا السياق أنّ الإيرادات غير الضريبيّة تمثل بشكل أساسي عائدات المؤسّسات المملوكة من الدولة مثل كازينو لبنان والمرافئ ومطار رفيق الحريري الدولي وقطاع الإتّصالات وغيرها. ويرفع قانون الموازنة عدّة غرامات بمعدّل 25 ضعفاً كما يشدّد متطلّبات الإبلاغ المتعلّقة بصاحب الحق الإقتصادي (وهو إجراء قد يساهم في مكافحة غسل الأموال والإمتثال بالمعايير الدولية) بحيث أصبح يتوجّب على المعنيين إبلاغ الجهات الضريبيّة المختصّة بأي تغيير في بيانات المالك المستفيد خلال مهلة شهر واحد (بدلاً من شهرين سابقاُ من تاريخ التغييير)، مع زيادة الرسوم المفروضة في حال عدم الإمتثال لهذه المتطلبات. كما يفرض القانون رسومًا على الشاحنات الأجنبية التي تعبر الأراضي اللبنانية لأغراض النقل الدولي، باستثناء الشاحنات التابعة لدول تعفي لبنان من هذه الرسوم بموجب اتفاقيات تجارة ثنائية. ويرفع قانون الموازنة نسبة العمولة المخصصة لبائعي الطوابع المالية إلى 7% (مقابل 5% سابقًا) من قيمة الطابع، بهدف تحفيزهم على بيع الطوابع بقيمتها الاسمية، كما يحدد الحد الأدنى للبدل اليومي للوجبات لموظفي القطاع الخاص عند 300,000 ليرة لبنانية. إضافةً إلى ذلك، ينص القانون على أن تقوم إدارة الجمارك بفرض رسم بنسبة 1.5% على كل عملية استيراد، على أن يُحتسب هذا المبلغ كسلفة على ضريبة الدخل للمستورد. وعلى صعيد الإيرادات أيضًا، تم رفع عدة رسوم مرتبطة بالمعاملات لدى المديرية العامة للأمن العام (بما في ذلك رسوم الإقامات لحاملي إجازات العمل). وقد فرض قانون الموازنة ضريبة إستثنائيّة نسبتها 17% على أرباح عمليّات صيرفة التي يتخطّى مجموعها ال100،000 د.أ. وأخيرًا، رفع القانون الغرامة المفروضة على شركات السياحة التي تنظم رحلات لمجموعات أجنبية عن كل شخص تحت مسؤوليتها يتخلّف عن مغادرة البلاد إلى 180 مليون ليرة لبنانية (مقابل 3 ملايين ليرة سابقًا).

أما على صعيد النفقات، فمن المتوقع أن تستحوذ المنافع الاجتماعية على أكثر من ربع إجمالي النفقات الموازنية (27.25%)، تليها الرواتب والأجور (23.66%)، ثم التحويلات (12.46%، ويُخصص جزء منها للرواتب والتحويلات إلى منظمات لا تبغي الربح). وتشمل بنود الإنفاق المهمة الأخرى النفقات الرأسمالية (11.96%)، لا سيما في شكل إستملاكات حكومية والمصاريف الإدارية (10.03%).

وعلاوةً على ذلك، خُصصت الحصة الأكبر من النفقات المرصودة لوزارة الدفاع الوطني (1.14 مليار دولار؛ 18.9%)، تليها مباشرة النفقات المشتركة (1.13 مليار دولار؛ 18.8%)، ثم وزارة الداخلية والبلديات (0.64 مليار دولار؛ 10.6%) ووزارة التربية والتعليم العالي (0.61 مليار دولار؛ 10.2%)، وذلك على سبيل المثال لا الحصر.