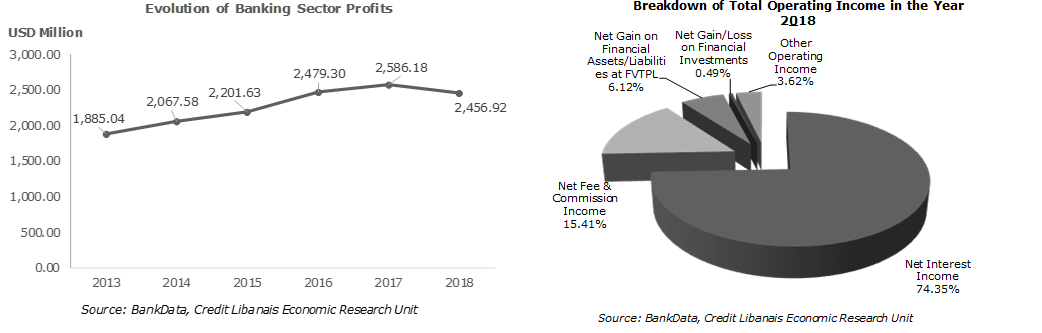

The consolidated net profit of the Lebanese banking sector was down by 5.00% in 2018 to just above $2.45 billion, as political tensions continued to cast their shadows on the country’s economic activity. Said drop can be attributed to the 1.62% contraction in net fees & commission income to $1.03 billion, coupled with the 54.69% dip in net gain on financial assets/liabilities at FVTPL, net gain on Financial Investments, and other operating income to $682.44 million, outweighing the 9.35% rise in net interest income to $4.96 billion. The year 2018 saw an extension of the financial engineering schemes launched by the Central Bank in mid-2016 whereby cash and balances with central banks rose by 33.8% ($27.83 billion) to $110.23 billion. The contraction in overall profitability can in part be attributed to the effect of the double taxation borne by banks, with tax on interest income from placements with central banks and in LBP-denominated treasury securities alone rising by 985% to $659.92 million and interest expense on customer deposit hiking by 19.4% to $11.49 billion as banks continued to raise interest rates to lure new deposits. Consequently, the return on average equity (ROaE) and return on average assets (ROaA) in the banking sector fell to 9.95% and 0.90% on a respective basis, while the capital adequacy ratio increased to 17.79%, up from 16.90% a year before.

Net interest income accounted for 74.35% of the consolidated banking sector’s operating income in the year 2018, followed by net commissions & fee income (15.41%) and net gains on financial assets/liabilities at FVTPL (6.12%), only to name a few.

Lebanese banks’ consolidated net profits have been building momentum at a compounded annual growth rate of 5.44% over the 2013-2018 period, from $1.89 billion in the year 2013 to $2.46 billion in the year 2018, reflecting as such the entrenched role of the sector as backbone of the economy.

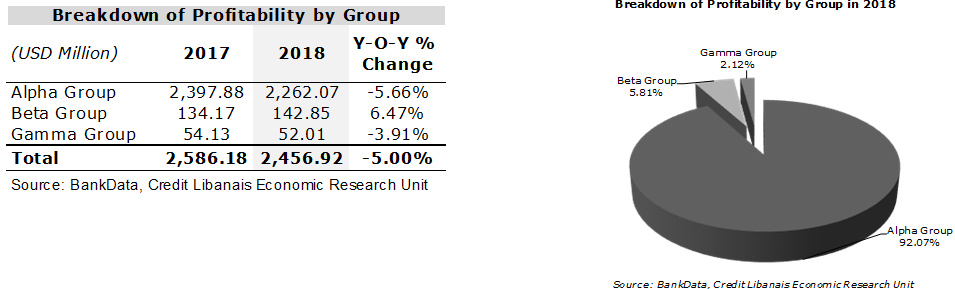

The profits of Alpha banks represented 92.07% of the consolidated profits of the Lebanese banking sector in 2018, followed by the Beta (5.81%) and Gamma (2.12%) groups. It is worth noting that Beta banks witnessed a 6.47% increase in profitability in 2018, while both Alpha and Gamma groups suffered respective drops of 5.66% and 3.91%.