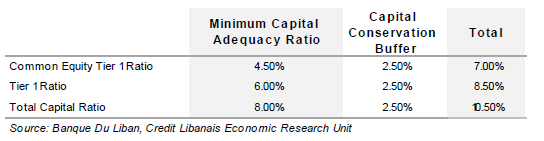

The Lebanese Central Bank issued on February 3, 2020 intermediate circulars no. 542 and 543 addressed to banks. In details, circular 543 requires banks to abide by the following solvency ratios.

In addition, the circular tied dividend distributions by banks to the satisfaction of certain thresholds, namely a 7% common equity tier 1 ratio, a 10% tier 1 ratio and a 12% total capital ratio. The circular also stipulates that banks must constitute a Capital Conservation Buffer of 2.5% of Risk Weighted Assets and that banks that fail in achieving said buffer must propose an action plan to the Banking Control Commission to build this threshold within a period of three years. Circular 543 also recommended adjusting the risk weight on Foreign Currency placements with BDL (including Certificates of Deposit) having a maturity of more than one year to 150%. The Central Bank specified in annex 6 of the circular the regulatory expected credit losses (ECLs) that will be applicable by banks in the calculation of the above Capital Adequacy Ratios. More specifically, an ECL of 1.89% will be applied on placements with the Central Bank in USD, 9.45% on USD placements with the government and on corporate loans for resident institutions among others, noting that an ECL of 0% will be applied on LBP placements with the government and with the Central Bank.

On its part, circular no. 542 stipulates that the expected accounting credit loss rates on placements with BDL (including Certificates of Deposit) and on sovereign placements must not exceed the regulatory credit loss rates mentioned above.

أصدر المصرف المركزي في 3 شباط 2019 التعميمين الوسيطين رقم 542 و534 الموجّهين إلى المصارف. بالتفاصيل، طلب التعميم رقم 543 من المصارف الإلتزام بنسب الملاءة التالية:

بالإضافة إلى ذلك، ربط التعميم توزيع أنصبة الأرباح لدى المصارف بتحقيقها نسب ملاءة معيّنة ألا وهي 7% على مستوى نسبة حقوق حملة الأسھم العادية و10% على مستوى الأموال الخاصة الأساسية و12% على مستوى نسبة الأموال الخاصة الإجماليّة. وقد أشار التعميم أيضاً أنّه يجب على المصارف تحقيق مستوى إحتياطي الحفاظ على الأموال الخاصة بنسبة 2.5% من الموجودات المرجحة بالمخاطر، وبأنّه يمكن للمصارف التي لا تتمكّن من تسجيل هذه النسبة تقديم خطّة عمل إلى لجنة الرقابة على المصارف لبلوغ هذه النسبة خلال 3 سنوات. أخيراً، أوصى التعميم رقم 543 بتعديل وزن مخاطر التوظيفات لدى مصرف لبنان (بما فيھا شھادات الإيداع) بالعملة الأجنبية بإستثناء تلك التي تبلغ آجالها أقل من سنة إلى 150%.وقد حدّد مصرف لبنان في الجدول رقم 6 نسب الخسائرالإئتمانيّة المتوقّعة نظاميّاً التي سوف تطبقها المصارف في إحتساب نسب الملاءة المذكورة أعلاه والمحددّة ب1.89% على التوظيفات مع مصرف لبنان بالعملة الأجنبيّة وب9.45% على التوظيفات بالعملة الأجنبيّة مع الحكومة وعلى التسليفات إلى الشركات المقيمة للذكر لا للحصر علماً أنّ نسبة 0% سوف تطبّق على التوظيفات بالليرة اللبنانيّة مع الحكومة والمصرف المركزي.

من جهّته، أشار التعميم رقم 542 إلى أنّ النسب المحاسبيّة (Accounting) لإحتساب الخسائر الإئتمانيّة المتوقّعة على التوظيفات مع مصرف لبنان ( بما فيھا شھادات الإيداع) والدولة اللبنانيّة يجب أن لا تتجاوز نسب الخسائر الإئتمانية المحتسبة نظاميّاً والمذكورة آنفاً.