Standard & Poor’s Global Ratings (S&P), the international rating agency, raised on February 13, 2026 Lebanon’s long-term local currency rating to “CCC+” from “CCC” previously while maintaining the country’s stable outlook. In the meantime, the rating agency maintained the country’s long-term and short-term foreign currency (FC) ratings at “SD”, and the short-term local currency (LC) rating at “C”. The rating agency attributed the rating upgrade to the government's improved ability to manage its local debt, thanks to three consecutive years of budget surpluses and progress achieved on the reforms needed for a new IMF program. According to the rating agency, Lebanon’s government has made some progress in passing laws that are considered as a prerequisite to unlock a new IMF financing program and moving ahead with debt restructuring. More specifically, S&P noted that the Cabinet has approved the Financial Stabilization and Deposit Repayment Act (a.k.a. the Gap Law) in December 2025 while at an earlier date in 2025 the Parliament ratified the amended Banking Secrecy Law and approved the Bank Restructuring Law. The rating agency stated that it expects reform progress to reduce funding constraints yet noted that said process would be gradual given the expected May 2026 elections along with the limited progress on other reforms, namely the medium-term fiscal framework and the amendments of banking laws to align them with international standards. In addition, S&P stated that Lebanon’s sovereign ratings show the government’s ability and willingness to service financial obligations to commercial creditors. Always in the same vein, the rating agency stated that it does not expect local currency debt to be included in a government debt-restructuring plan under its base-case scenario. In addition, S&P commented that the 98% depreciation of the Lebanese pound since the onset of the crisis in late 2019 has sharply reduced the value of LBP-denominated debt to below 1% of GDP (or ~1% of gross general government debt) at end of 2025. The agency also mentioned that the Lebanese government had stopped making interest payments on local currency debt to BDL between the years 2021 and 2023, yet these payments resumed in 2024 and all accrued interest was settled in 2025. S&P commented that it could lower the LC rating within the next twelve months in the event of increased odds of the inclusion of local currency debt in a restructuring exercise, while ratings can be upwardly revisited in the event additional progress is achieved on reforms that would eventually lead to better fiscal results, economic growth, and pave the way to concessional external funding.

On the other hand, the rating agency commented that it considers the policy challenges for Lebanon as substantial. In details, and given the small timeframe until parliamentary elections in May 2026 alongside the uncertainty surrounding the precise timing of elections, S&P noted that it does not expect any major progress on debt restructuring in the near-term. The agency highlighted that what aggravated the country’s recovery journey is the latest conflict with Israel, which affected Lebanon’s economic prospects, bearing in mind that the implementation of the November 2024’s ceasefire remains fragile. In parallel, the rating agency stated that it does not expect major progress on public debt restructuring in 2026 considering the slow progress on banking sector reforms and deposits recovery. Furthermore, and despite the unstable security situation, S&P expects the Lebanese economy to grow slowly due to a stronger reconstruction activity, a promising tourism sector recovery, and improved political environment.

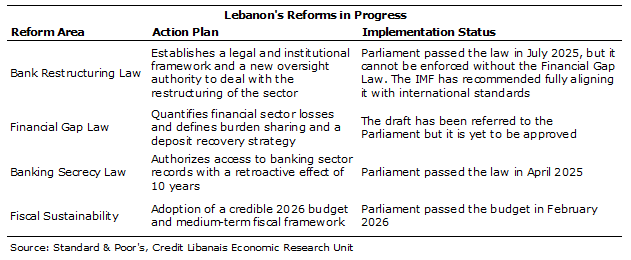

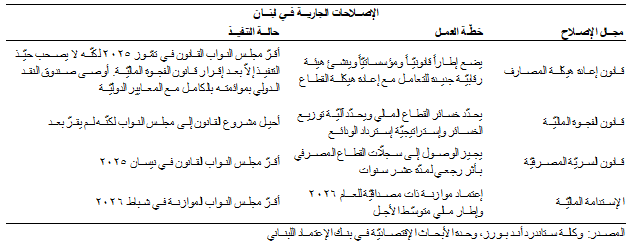

The rating agency mentioned that it expects the Lebanese authorities to continue prioritizing reforms that target rebuilding the economy and improving governance. The agency added that since the formation of the government in early 2025, the latter has achieved remarkable progress on a set of reforms required for a potential IMF board approval of an Extended Fund Facility Program, the details of which are provided in the table below:

The rating agency also pinpointed a list of other reforms required to unlock external financing such as a medium-term fiscal plan, a banking sector restructuring law, reforming state-owned enterprises, and strengthening the Anti-Money Laundering & Combating the Financing of Terrorism legislation. Reforms execution risk remains elevated, however, according to the agency given the short timeframe before the parliamentary elections in May 2026 and strained security situation with Israel.

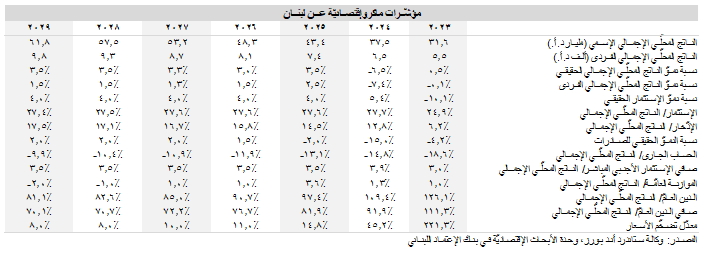

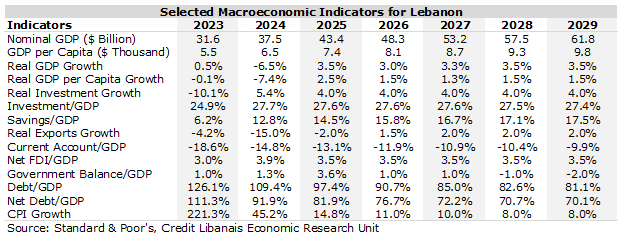

Standard & Poor’s added that barring the slight post-pandemic rebound in the 2021-2023 period, the country’s economy has been contracting in real terms since 2018, with real GDP shrinking from $55 billion in 2018 to $37.5 billion in 2024. S&P estimated GDP however to have expanded by about 3.5% in real terms in 2025 after having contracted by 6.5% in 2024. In the same vein, the rating agency expects economic growth to remain somewhat stable in the 2026-2029 forecast period fueled by a diversified service sector recovery and consumption, as well as improved liquidity conditions due to rising fresh Dollar withdrawal limits and strong influx of remittances. The rating agency added that the official exchange rate has been stable at the LBP 89,500/USD level since February 2024. S&P stated that it expects the exchange rate to remain mostly stable in 2026 followed by a “modest depreciation”. In addition, the agency noted that it expects net general government debt as a percentage of GDP to continue its gradual decline, dropping from 232.9% in 2022 to 81.9% in 2025 and a projected 76.7% in 2026.

S&P added that it excludes gold and some $7 billion of banks’ required reserves on FC deposits from gross reserves to arrive at usable reserves. In the same vein, the rating agency stated that gross reserves (including gold) stood at circa $54 billion as at January 15, 2026, of which some $12 billion are in the form of liquid foreign assets. According to S&P, Lebanese laws prohibit the sale of BDL’s gold holdings unless the Parliament ratifies a new law to allow the sale of gold and hence S&P views that gold is not readily available for foreign exchange operations and repayment of external debt. S&P projected the current account deficit to drop to an average of 11% over the 2026-2029 period, from an average of 16% over the 2023-2025 period, yet commented that this figure remains elevated and can be financed by remittances and resident foreign currency savings. Finally, the rating agency pointed out that average annual inflation ebbed to 14.8% in 2025 down from 221.3% in 2023, while expecting inflation to remain below 10% in the 2028-2029 period.

رفعت وكالة التصنيف الدوليّة ستاندرد أند بورز (S&P Global Ratings) في 13 شباط 2026 تصنيف لبنان بالعملة المحليّة على المدى الطويل من "CCC" إلى "CCC+" مع نظرة مستقبليّة مستقرّة. في الوقت عينه، أبقت الوكالة على التصنيف الطويل والقصير الأمد للديون السياديّة بالعملات الأجنبيّة عند التخلّف الإنتقائي عن الدفع "Selective Default" وتصنيف العملة المحليّة على المدى القصير عند "C". وعزت الوكالة رفع التصنيف إلى تحسّن قدرة الحكومة على إدارة دينها المحلّي بفضل الفوائض المحقّقة في الموازنة لثلاثة أعوام متتالية والتقدّم المحرز في الإصلاحات المطلوبة من صندوق النقد الدولي. وبحسب وكالة التصنيف، فقد حقّقت الحكومة اللبنانيّة بعض التقدّم لجهة إعتماد قوانين تُعتَبَر شروط مسبقة للتوصّل إلى إبرام إتفاقيّة مع صندوق النقد والتقدّم في إعادة هيكلة الدين. بالتفاصيل، أشارت وكالة ستاندرد أند بورز أنّ مجلس الوزراء قد وافق على قانون الفجوة الماليّة في شهر كانون الأوّل 2025 وأحالة إلى مجلس النواب لإقراره علماً أنّ البرلمان كان قد صادق في العام 2025 على قانون السريّة المصرفيّة المعدّل وعلى قانون إعادة هيكلة المصارف. وقد أشارت وكالة التصنيف أنّها تتوقّع أن يحدّ التقدّم في الإصلاحات من القيود على التمويل إلاّ أنّها أشارت إلى أنّ هذه العمليّة ستكون تدريجيّة على ضوء نتائج الإنتخابات النيابيّة المرتقبة في أيّار 2026 تزامناً مع التقدّم المحدود المحرز على إصلاحات أخرى كالإطار المالي المتوسّط الأجل والتعديلات على القوانين المصرفيّة للتماشي مع المعايير الدوليّة. بالإضافة إلى ذلك، أشارت وكالة ستاندرد أند بورز أنّ تصنيفات لبنان السياديّة تظهر قدرة وإستعداد الحكومة للإيفاء بالإلتزامات الماليّة تجاه الدائنين التجاريّين. وفي السياق نفسه، ذكرت وكالة ستاندارد آند بورز بأنّها لا تتوقّع إدراج الدين بالعملة المحليّة من ضمن خطّة إعادة هيكلة الدين الحكومي في إطار سيناريو توقّعاتها المعتمد (Base Case Scenario). وقد علّقت الوكالة بأنّ تدهور سعر صرف الليرة اللبنانيّة مقابل الدولار الأميركي بنسبة 98% قد أدّى إلى تراجع كبير في قيمة الدين المقوّم بالليرة اللبنانيّة إلى أقلّ من 1% من الناتج المحلّي الإجمالي (أو حوالي 1% من إجمالي الدين الحكومي) كما في نهاية العام 2025. وأضافت وكالة التصنيف الائتماني أنه في حين أنّ الحكومة توقّفت عن دفع مستحقّاتها بالليرة اللبنانيّة للبنك المركزي بين عاميّ 2021 و2023، إلا أنّها إستأنفت هذه الدفعات في العام 2024 وسدّدت الدفعات المتراكمة المتبقّية خلال العام 2025. وعلّقت وكالة ستاندرد آند بورز بأنها قد تخفّض تصنيف الدين بالعملة المحليّة في الأشهر ال12 القادمة في حال زيادة إحتمال إدراج الدين بالعملة المحليّة من ضمن عمليّة إعادة الهيكلة، في حين أنّها قد ترفع التصنيف أكثر في حال تحقيق تقدّم إضافي في الإصلاحات التي من شأنها أن تؤدي في نهاية المطاف إلى نتائج أفضل للماليّة العامّة ونموّ إقتصادي وفتح الباب أمام تمويل خارجي بشروط ميسّرة.

من جهةٍ أخرى، إعتبرت وكالة التصنيف أنّ تحديات السياسات في لبنان كبيرة. بالتفاصيل، ونظراً إلى الإطار الزمني المحدود قبل إجراء الإنتخابات النيابيّة في أيّار 2026 ترافقاً مع حالة عدم اليقين حول موعد الإنتخابات، أشارت وكالة ستاندرد أند بورز أنّها لا تتوقّع تقدّم ملموس لناحية إعادة هيكلة الدين العامّ على المدى القريب. وقد ذكرت الوكالة أنّ العدوان الأخير على لبنان قد فاقم من حدّة الأزمة التي تمرّ بها البلاد، ما ألقى بثقله على آفاق لبنان الإقتصاديّة، علماً أنّ التطبيق لإتفاقيّة وقف إطلاق النار منذ شهر تشرين الثاني 2024 لا يزال هشّاً. في المقابل، أشارت وكالة ستاندرد أند بورز أنّها لا تتوقّع تقدّم ملحوظ لناحية إعادة هيكلة الدين العامّ في العام 2026 نظراً إلى التقدّم البطيء في إصلاح القطاع المصرفي وإستعادة الودائع. بالإضافة إلى ذلك، وبالرغم من الوضع الأمني المتقلّب، توقّعت الوكالة أنّ ينمو الإقتصاد اللبناني بشكلٍ خجول مدعوماً بحركة إعادة إعمار قويّة وتعافي واعد لقطاع السياحة والتحسّن في المشهد السياسي.

وقد أشارت وكالة التصنيف أنّها تتوقّع أن تلتزم السلطات في لبنان بإعطاء الأولويّة للإصلاحات التي تستهدف إعادة بناء الإقتصاد وتحسين الحوكمة. وبحسب وكالة ستاندرد أند بورز، ومنذ تشكيل الحكومة في أوائل العام 2025، أحرزت هذه الأخيرة تقدّم ملحوظ لجهة عدد من الإصلاحات المطلوبة للإستحصال على تمويل من قبل صندوق النقد الدولي كما هو مفصّل أدناه:

وقد أفادت وكالة التصنيف عن إصلاحات أخرى مطلوبة لتحرير تمويل خارجيّ كخطّة ماليّة متوسّطة الأجل وقانون إعادة هيكلة المصارف وإصلاح الشركات المملوكة من الدولة وتعزيز تشريعات مكافحة غسل الأموال وتمويل الإرهاب. ومع ذلك، فلا تزال مخاطر التنفيذ مرتفعةً وفقاً للوكالة، نظراً لضيق الوقت قبل الإنتخابات البرلمانيّة في أيّار 2026 والوضع الأمني المتوتر مع إسرائيل.

وأضافت وكالة ستاندرد آند بورز أنّه بإستثناء الإنتعاش الطفيف المسجّل بعد جائحة كورونا بين الأعوام 2021 و2023، فإنّ الإقتصاد اللبناني قد إستمّر بالتراجع منذ العام 2018، مع إنكماش الناتج المحلّي الإجمالي الحقيقي من 55 مليار د.أ. في العام 2018 إلى 37.5 مليار د.أ. في العام 2024. وقد قدّرت الوكالة بأن يكون الناتج المحلّي الإجمالي الحقيقي قد إرتفع بنسبة 3.5% في العام 2025 بعدما كان قد إنكمش بنسبة 6.5% في العام 2024. في الإطار نفسه، توقّعت وكالة ستاندرد أند بورز أن يبقى النموّ في الناتج المحلّي الإجمالي الحقيقي مستقرّاً بعض الشيئ خلال الفترة الممتدّة بين الأعوام 2026 و2029 نتيجة إنتعاش قطاع الخدمات والإستهلاك إضافةً إلى التحسّن في مستوى السيولة بسبب رفع سقوف السحوبات بالدولار الفريش وتدفّق قويّ للتحويلات الماليّة. وأضافت وكالة التصنيف بأنّ سعر الصرف الرسمي قد بقي مستقراً عند مستوى 89،500 ليرة لبنانيّة مقابل الدولار الأميركي منذ شهر شباط 2024. وقد أشارت الوكالة أيضاً أنّها تتوقّع أن يبقى سعر الصرف مستقرّاً خلال العام 2026 ليتبعه تراجع بسيط في الفترة اللاحقة. بالإضافة إلى ذلك، توقّعت الوكالة أن يستمرّ التراجع في صافي الدين كنسبة من الناتج المحلي الإجمالي من 232.9% في العام 2022 إلى 81.9% في العام 2025 و76.7% في العام 2026.

وقد أضافت وكالة ستاندرد أند بورز أنّها لا تدخل في إحتساب إجمالي الإحتياطات لدى مصرف لبنان قيمة الذهب والإحتياطات الإلزاميّة على الودائع بالعملة الأجنبيّة (والمقدّرة بحوالي 7 مليار د.أ.) للوصول إلى الإحتياطات القابلة للإستعمال. في الإطار نفسه، أشارت وكالة التصنيف أنّ إجمالي الإحتياطات (والتي تشمل الذهب) قد بلغت 54 مليار د.أ. كما في 15 كانون الثاني 2026 وهي تشمل حوالي 12 مليار د.أ. على شكل إحتياطات بالعملة الأجنبيّة قابلة للإستعمال. وبحسب وكالة ستاندرد أند بورز، فإنّ القوانين اللبنانيّة تمنع بيع ذهب مصرف لبنان إلاّ في حال شرّع البرلمان قانون جديد يسمح ببيع الذهب وبالتالي ترى الوكالة أنّ الذهب حاليّاً ليس جاهزاً لعمليّات صرف بالعملات الأجنبيّة وإعادة تسديد الدين الخارجي. وتوقّعت وكالة ستاندرد آند بورز بأن ينخفض متوسّط العجز في الحساب الجاري إلى 11٪ من الناتج المحلّي الإجمالي خلال الفترة الممتدّة بين عاميّ 2026 و2029، من 16٪ خلال الفترة الممتدّة بين عاميّ 2023 و2025، إلا أنّها علّقت بأنّ هذا العجز لا يزال مرتفعاً ويمكن تمويله من تحويلات المغتربين الوافدة إلى لبنان ومن إدخارات القطاع الخاصّ المقيم بالعملة الأجنبيّة. وأخيراً، أشارت وكالة التصنيف الائتماني إلى أن متوسّط التضخّم السنوي قد إنخفض إلى 14.8% في العام 2025 من 221.3% في العام 2023، كما وتوقّعت بأن يبقى المتوسّط أدنى من نسبة ال10% في الأعوام 2028 و2029.