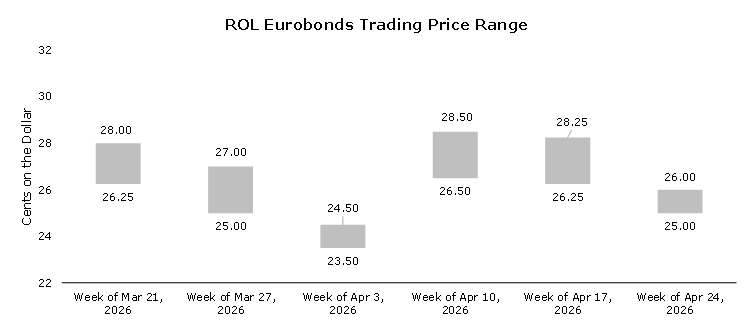

Lebanese Eurobond prices retreated this week as market activity remained subdued, characterized by thin liquidity and sellers outweighing a limited number of buyers. Firm bids were mainly concentrated around 25.00–26.00 cents on the dollar (below market indications), reflecting a cautious stance across the curve. Overall, participants are still adopting a wait-and-see approach, closely monitoring developments, particularly any potential positive signals from US–Iran negotiations that could improve risk sentiment and pricing. Despite the fact that the Lebanon–Israel talks in Washington reached an agreement to extend the truce for another three weeks, prices didn’t improve and market appears to be looking beyond the near-term extension to the progress on longer-term diplomatic outcomes, including a path toward ending the US war with Iran.

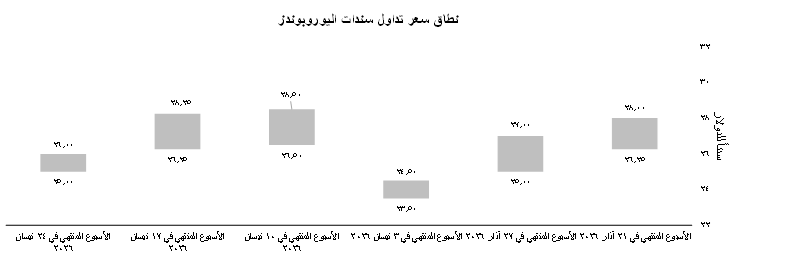

تراجعت أسعار سندات اليوروبوندز اللبنانيّة هذا الأسبوع مع إستمرار ضعف النشاط السوقي الذي إتّسم بإنخفاض السيولة وإرتفاع مستوات العرض مقابل الطلب. وتركّزت العروض الجديّة بشكل رئيسي حول مستوى 25.00-26.00 سنتاً للدولار أي أقلّ من مؤشّرات السوق، مما يعكس نهجاً حذراً يسود كامل منحنى العائد (Yield Curve). بشكل عام لا يزال المستثمرون يتبنّون نهج الترقّب والإنتظار (Wait and See) ويراقبون التطوّرات عن كثب لا سيما أيّ إشارات إيجابيّة محتملة من المفاوضات الأمريكيّة الإيرانية التي قد تُحسّن معنويات المخاطرة (risk sentiment) والأسعار. وعلى الرغم من أنّ المحادثات اللبنانيّة الإسرائيليّة في واشنطن قد توصلت إلى إتّفاق لتمديد الهدنة لثلاثة أسابيع أخرى، إلا أنّ ذلك لم ينعكس على مستويات الأسعار، بحيث يبدو بأنّ السوق يتطلّع إلى ما هو أبعد من التمديد القصير الأجل، وخاصّةً نحو تقدم في النتائج الدبلوماسيّة الطويلة الأجل، بما في ذلك إيجاد سبيل لإنهاء الحرب الأمريكيّة مع إيران.