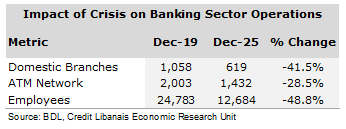

Banque Du Liban’s recent Macroeconomic Review publication which covers the full year 2025 shed light on the current situation of the banking sector pointing out that the sector currently comprises 57 banks, of which 45 commercial (36 Lebanese-owned down from 38 at the start of the crisis and 9 foreign-owned) and 12 investment banks (down from 16 pre-crisis). The review added that banks were compelled into downsizing their operations as a result of the crisis, whether in terms of domestic branches which were reduced by 439 between 2019 and 2025 (41.5%) to 619 (and down by 2.21% in 2025 alone from 633 branches in 2024), ATM network which contracted by 571 machines between the years 2019 and 2025 (28.5%) to 1,432 (noting it increased by 1.42% in 2025 alone from 1,412 machines in 2024) or taskforce which fell by 12,099 employees (48.8% between 2019 and 2025) to 12,684. This is further outlined by the below table:

The crisis also had a profound impact on major elements of commercial banks’ balance sheet as highlighted by the below section:

- Assets: According to BDL, the structure of commercial banks’ assets in 2025 is still heavily concentrated in placements with BDL, reaffirming the dominance of sovereign exposures on banks’ balance sheets. More specifically, currency and deposits at BDL are still the largest asset component standing at $77.5 billion in 2025 down from $79.6 billion in 2024, accounting for 76% of total assets. The securities portfolio fell from $7.1 billion in December 2024 to $6.7 billion in December 2025 (4.3% decline) mainly on the back of the contraction in the resident securities portfolio from $6.25 billion to $5.34 billion in 2025, which was partly offset by the increase in the non-resident securities portfolio from $805.1 million to $1,413.8 million over the same period.

- Loans: BDL noted that credit creation is still largely impaired as evidenced by the 12.5% y-o-y contraction in total claims to $5.2 billion in December 2025 down from $5.9 billion in December 2024. The majority of loans (98%) are denominated in foreign currency while the remaining 2% is denominated in Lebanese Pound. The report noted that despite the 10% and 13% drops in LBP and USD claims in 2025, the pace of decline has dropped compared to the 29% contraction witnessed in 2024. In addition, total loans fell from $58.1 billion in January 2019 (23% of banking sector assets and 109% of GDP) to $5.2 billion in December 2025 (5.1% of assets and circa 16% of GDP). Concerning fresh loans, their activity expanded significantly in 2025, rising from $418 million in December 2024 to $794 million in December 2025, representing a 90% increase. BDL noted however that despite this increase, the volume of fresh lending remains small, representing circa 2.5% of the country’s nominal GDP.

- Asset Quality: BDL commented that from February until October 2025, the banking sector continued to display a weak asset profile with Non-Performing Loans (NPLs) remaining pervasive across all loan sizes. In figures, the NPL ratio reached 86.3% in October 2025, remaining unchanged from February 2025’s reading. The ratio of NPLs rose significantly between December 2019 and October 2025 across several loan tranches. Nevertheless, the NPL ratio dropped from 78.4% in February 2025 to 69.9% in October for loans under LBP 10 billion, from 83.4% to 80.0% for loans under LBP 20 billion, from 86.7% to 85.8% for loans below LBP 30 billion, and from 85.1% to 84.6% for tranches below LBP 40 billion. On the other hand, the NPL ratio increased from 86.8% in February 2025 to 88.0% in October for tranches under LBP 50 billion while also increasing from 86.8% to 87.4% for loans above LBP 50 billion.

- Deposits: The size of the deposit portfolio fell from $172.1 billion in June 2019 ($123.1 billion in FC deposits and $49.1 billion in LC deposits) to $88.6 billion in December 2024 ($87.9 billion in FC deposits and $0.8 billion in LC deposits) and $87.2 billion in December 2025 ($86.2 billion in FC deposits of which $5 billion in fresh deposits up to November and $1 billion in LC deposits). According to BDL, the $1.5 billion drop witnessed in 2025 owes mainly to the reduction of FC deposits amid continued withdrawals of frozen deposits. BDL commented that the partial repayment of FC deposits has increased in 2025, rising from $4.1 billion in the first half of 2025 to $5.3 billion in the full year 2025, noting that repayments under BDL circular 158 rose by 46% y-o-y, those under BDL circular 166 increased by 199%, and those under both circulars rising by 71.2% over the concerned period. As far as fresh deposits are concerned, the review revealed that the size of fresh deposits has attained $5.0 billion in November 2025 up from $3.5 billion in December 2024, reflecting a rise of circa $1.5 billion. The report noted however that this $1.5 billion increase reflects balances accumulated under circulars 158 and 166 (which rose from $1.9 billion to $3.2 billion). When excluding the circular-related balances, liquid fresh deposits would have risen from $1.6 billion to $1.9 billion (increase of $283 million).

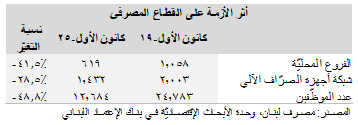

ألقت النشرة الثانية من المراجعة الكليّة الإقتصاديّة التي أصدرها مصرف لبنان مؤخّراً عن كامل العام 2025 الضوء على الوضع الحالي للقطاع المصرفي. وأشار التقرير أولاً إلى أنّ القطاع المصرفي اللبناني يضم 57 مصرفاً، منها 45 مصرفاً تجاريّاً (36 مصرفاّ مملوكاً من لبنانيين بإنخفاض عن 38 في بداية الأزمة و9 مصارف مملوكة من أجانب) و12 مصرف إستثمار (بانخفاض عن 16 قبل الأزمة). وأضاف التقرير بأنّ المصارف قد إضطرّت إلى تقليص عمليّاتها نتيجة الأزمة، أكان لجهة عدد الفروع المحليّة التي إنخفضت بمقدار 439 فرعاً (41.5%) إلى 619 فرعاً في نهاية العام 2025 (وتراجعت بنسبة 2.21% في العام 2025 وحده من 633 فرعاً في نهاية العام 2024) أو شبكة أجهزة الصرّاف الآلي التي تراجعت بمقدار 571 جهازاً (28.5٪) بين عاميّ 2019 و2025 إلى 1،432 (علماً أنّها زادت بنسبة 1.42% في العام 2025 من 1،412) أو اليد العاملة التي إنخفضت بمقدار 12،099 موظّفاً (48.8٪ منذ إندلاع الأزمة) إلى 12،684 كما هو موضح في الجدول أدناه:

وقد كان للأزمة أيضاً أثر بالغ على العناصر الرئيسيّة في ميزانيّة المصارف التجاريّة، كما هو موضح في القسم التالي:

- الموجودات: بحسب مصرف لبنان، لا تزال موجودات القطاع المصرفي في العام 2025 تتركّز في التوظيفات لدى مصرف لبنان، ممّا يعيد التأكيد على الإنكشافات السياديّة على ميزانيّات المصارف. بالتفاصيل، لا تزال الودائع والنقد لدى مصرف لبنان أكبر مكوّن على ميزانيّة المصارف حيث تراجعت إلى 77.5 مليار د.أ. في العام 2025 من 79.6 مليار د.أ. في العام 2024 (وهي تشكّل 76% من إجمالي الموجودات).وقد اراجعت محفظة الأوراق الماليّة من 7.1 مليار د.أ. في العام 2024 إلى 6.7 مليار د.أ. في نهاية العام 2025 (تراجع بنسبة 4.3%) وذلك نتيجة تراجع المحفظة المحليّة من 6.25 مليار د.أ. إلى 5.34 مليار د.أ. في العام 2025 والتي قوبلت جزئيّاً بإرتفاع محفظة الأدوات الماليّة الخارجيّة من 805.1 مليون د.أ. إلى 1،413.8 مليون د.أ. في الفترة نفسها.

- محفظة القروض: أشار مصرف لبنان إلى أنّ حركة التسليف لا تزال خجولة كما هو مبيّن من خلال الإنكماش السنويّ بنسبة 12.5% في محفظة القروض إلى 5.2 مليار د.أ. في كانون الأوّل 2025 من 5.9 مليار د.أ. في كانون الأوّل 2024. تتركّز القروض بالعملة الأجنبيّة (98%) في حين أنّ حصّة القروض بالعملة المحليّة هي 2% فقط. وقد أشار التقرير أنّه بالرغم من تراجع التسليفات بالليرة بنسبة 10% وتلك بالدولار الأميركي بنسبة 13% في العام 2025، فإنّ وتيرة التراجع قد إنكمشت مقارنةً بالإنخفاض المسجّل في العام 2024 والبالغ 29%. بالإضافة إلى ذلك، فقد تراجعت محفظة القروض من 58.1 مليار د.أ. في كانون الثاني 2019 (وهي تشكّل 23% من موجودات المصارف و109% من الناتج المحلّي الإجمالي) إلى 5.2 مليار د.أ. في كانون الأوّل 2025 (وهي تشكّل 5.1% من إجمالي الموجودات و16% من الناتج المحلّي الإجمالي). أمّا بالنسبة للقروض المعنونة بالدولار الفريش، فقد توسّع نشاطها بشكلٍ بارز خلال العام 2025 حيث زادت من 418 مليون د.أ. في العام 2024 إلى 794 مليون د.أ. في كانون الأوّل 2025 أي ما يشكّل زيادة نسبتها 90%. وقد أشار مصرف لبنان أنّه بالرغم من هذا الإرتفاع، فإنّ حجم الإقراض بالدولار الفريش لا يزال صغيراً إذ يشكّل حوالي 2.5% من الناتج المحلّي الإجمالي الإسمي للبلاد.

- جودة الأصول: أشار مصرف لبنان إلى أنّه خلال الفترة الممتدّة بين شباط 2025 وتشرين الأوّل 2025، واصل القطاع المصرفي إظهار ضعف في نوعيّة الأصول مع بقاء القروض المتعثّرة (Non-Performing Loans) منتشرة ضمن جميع فئات القروض. بالأرقام، بلغت نسبة القروض المتعثّرة 86.3% في تشرين الأوّل 2025 وهي النسبة نفسها مقارنةً بأرقام شهر شباط. وقد إرتفعت نسبة القروض المتعثّرة بشكلٍ بارز بين كانون الأوّل 2019 وتشرين الأوّل 2025 في عدّة شرائح من القروض. ومع ذلك، فقد تراجعت نسبة القروض المتعثّرة من 78.4% في شباط 2025 إلى 69.9% في تشرين الأوّل للقروض التي تقلّ قيمتها عن ال10 مليار ل.ل. ومن 83.4% إلى 80.0% للقروض التي تقلّ قيمتها عن ال20 مليار ل.ل. ومن 86.7% إلى 85.8% للقروض التي تقلّ قيمتها عن ال30 مليار ل.ل. ومن 85.1% إلى 84.6% للقروض التي تقلّ قيمتها عن ال40 مليار ل.ل. في المقابل، إرتفعت نسبة القروض المتعثّرة من 86.8% في شباط 2025 إلى 88.0% في تشرين الأوّل 2025 للقروض التي تقلّ قيمتها عن ال50 مليار ل.ل. ومن 86.8% إلى 87.4% للقروض التي تفوق قيمتها ال50 مليار ل.ل.

- الودائع: تراجع حجم محفظة الودائع من 172.1 مليار د.أ. في حزيران 2019 (123.1 مليار د.أ. منها ودائع بالعملات الأجنبيّة و49.1 مليار د.أ. ودائع بالعملة المحليّة) إلى 88.6 مليار د.أ. في كانون الأوّل 2024 (87.9 مليار د.أ. منها ودائع بالعملات الأجنبيّة و0.8 مليار د.أ. ودائع بالعملة المحليّة) وإلى 87.2 مليار د.أ. في كانون الأوّل 2025 (86.2 مليار د.أ. منها ودائع بالعملات الأجنبيّة و1.0 مليار د.أ. ودائع بالعملة المحليّة). وبحسب مصرف لبنان، فإنّ الإنخفاض البالغ 1.5 مليار د.أ.المسجّل في العام 2025 يعود إلى تراجع الودائع بالعملات الأجنبيّة في ظلّ إستمرار سحوبات الودائع المجمّدة. وقد علّق مصرف لبنان أنّ السداد الجزئي لتلك الودائع بالعملة الأجنبيّة قد زاد في العام 2025 من 4.1 مليار د.أ. في النصف الأوّل من العام 2025 إلى 5.3 مليار د.أ. في كامل العام 2025، علماً أنّ السحوبات بموجب التعميم رقم 158 قد إرتفعت بنسبة 46% سنويّأً وتلك تحت إطار التعميم 166 قد زادت بنسبة 199% وتلك بموجب التعميمين قد إرتفعت بنسبة 71.2% في الفترة المعنيّة. فيما يتعلق بالودائع الفريش، كشف مصرف لبنان بأنّ حجمها قد بلغ 5.0 مليار د.أ. في نهاية تشرين الثاني 2025 (من 3.5 مليار د.أ. في كانون الأوّل 2024) ما يعكس زيادة بقيمة 1.5 مليار د.أ. وقد أشار التقرير أنّ هذا الإرتفاع يعكس أرصدة متراكمة تحت إطار التعميمين 158 و166 (والتي زادت من 1.9 مليار د.أ. إلى 3.2 مليار د.أ.). وعند إستثناء الأرصدة المرتبطة بتلك التعاميم، فإنّ الودائع الفريش السائلة كانت لترتفع من 1.6 مليار د.أ. إلى 1.9 مليار د.أ. (أيّ زيادة ب283 مليون د.أ.).