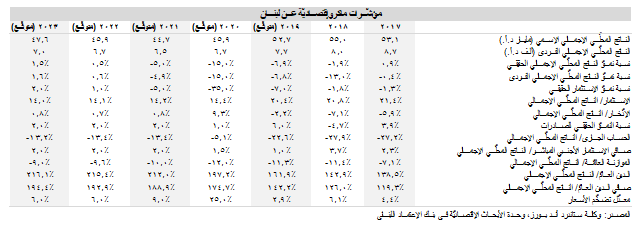

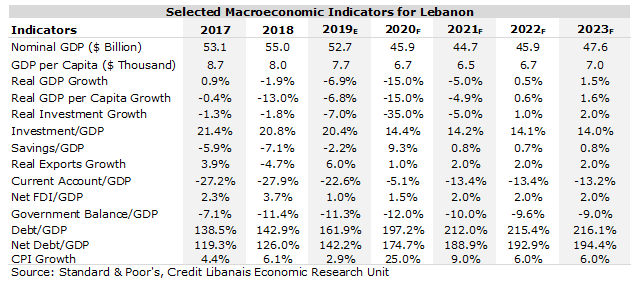

Standard & Poor’s Global Ratings (S&P), the international rating agency, lowered the rating of several Lebanese Eurobonds to “D” (Default) from “SD” (Selective Default) on a missed principal payment (being the third Eurobond principal repayment) that was due on June 19, 2020, in addition to missed interest payments that were due in March and April. The agency also affirmed the long and short-term foreign currency (FC) ratings at “SD”, and the long and short-term local currency ratings at “CC” and “C” respectively. The outlook for local currency debt is still negative, portraying the probability that the Lebanese Government to opt to restructure its local currency debt. S&P kept Lebanon’s transfer and convertibility assessment stable at “CC”. In addition, the agency lowered the issue ratings from “CC” to “D” on several bonds with coupon payments due in May and June. The details of said bonds are portrayed in the below table:

The rating agency highlighted that the Government has made little progress in engaging creditors in debt-restructuring negotiations. In this vein, the agency expects the negotiations to be delayed beyond the year 2020 in the absence of a consensus over the comprehensive reform plan, not to mention the COVID-19 pandemic which also added ramifications to the already frail economic activity along with harsh external, fiscal, and financial constraints. From another standpoint, the report pointed to the faltering local currency peg to the dollar amid the ongoing foreign currency shortages and the widening gap between the official and parallel exchange rates. According to S&P, a restructuring program could entail an official currency devaluation, noting that the Government has not decided to this date on restructuring its local currency debt obligations standing at around 110% of GDP, yet stated that the Government would have to restructure the said debt if it where to put it on a sustainable path. In this respect, the agency commented that it foresees a high probability of a domestic debt restructuring in order to lower public debt to sustainable levels.

The rating agency stated that it could improve the foreign currency issuer credit and issue ratings for Lebanon from “SD” and “D” following the completion of the Government’s bond restructuring plans. Finally, the agency commented that it could improve the sovereign rating if the probability of a distressed exchange of Lebanon’s local currency debt decreases. S&P stated as well that it could lower the local currency issuer rating to “SD” if the government signals its intention to restructure its local currency debt.

خفّضت وكالة التصنيف الدوليّة ستاندرد أند بورز (S&P Global Ratings) تصنيف عدّة سندات سياديّة لبنانيّة إلى تعثّر "D" من تخلّف تلقائي عن الدفع "SD"، على إثر عدم سداد دفعة أصل دين إستحقّت بتاريخ 19 حزيران 2020، إضافةً إلى التخلّف عن سداد دفعات قسائم إستحقّت خلال شهريّ آذار ونيسان. من ناحية أخرى، قامت الوكالة بإبقاء التصنيف الطويل والقصير الأمد للديون السياديّة بالعملات الأجنبيّة عند "SD" محافظةً كذلك على التصنيف الطويل والقصير الأمد للديون السياديّة بالعملات المحليّة عند "CC" و"C" بالتتالي مع نظرة مستقبليّة سلبيّة. وقد عزت الوكالة النظرة المستقبليّة السلبيّة للدين بالعملة المحليّة إلى الشكوك التي تحوم حول إحتماليّة قيام الحكومة اللبنانيّة بإعادة هيكلة هذا الدين. بالإضافة إلى ذلك، أبقت الوكالة تقييم لبنان للنقل والتحويل "transfer and convertibility assessment" عند "CC".كما وخفّضت الوكالة تصنيف عدّة سندات إستحقّت قسائمها في شهر أيّار وشهر حزيران من "CC" إلى "D". هذه السندات مفصّلة في الجدول التالي:

وقد لفتت الوكالة إلى أنّ الحكومة لم تحرز تقدّماً ملموساً بالمفاوضات مع دائنيها. في هذا الإطار، توقّعت الوكالة بأن تتأجّل المفاوضات إلى ما بعد العام 2020 نتيجة عدم وجود إجماع حول الخطّة، ناهيك عن إنتشار وباء كورونا الذي ألقى بتداعياته على حركة الإقتصاد الهشّ إضافةً إلى قيود خارجيّة، ونقديّة، وماليّة. وقد لفتت الوكالة النظر إلى تدهور سعر الصرف نتيجة تضاؤل الإحتياطات بالعملة الأجنبيّة وإلى إتسّاع الهوّة بين سعر الصرف الرسمي وسعر الصرف في السوق السوداء. وبحسب الوكالة، فإنّ مشروع إعادة هيكلة الدين بالعملات المحليّة قد يتسبّب بإنهيار سعر الصرف، علماً أنّ الحكومة اللبنانيّة لم تصل إلى قرار بعد حيال دفع سندات الدين بالعملة المحليّة والتي تشكّل حوالي ال110% من الناتج المحلّي الإجمالي، إلّا أنّ الوكالة قد أشارت إلى أنّ الحكومة ستضطّر إلى إعادة هيكلة دينها في حال أرادت وضعه على المسار الصحيح.

أخيراً، أشارت الوكالة إلى أنّها ستقوم بتحسين تصنيف الدين بالعملة الأجنبيّة في حال نجحت خطّة الحكومة لإعادة هيكلة سندات الدين. وقد لفتت الوكالة أيضاً بأنها ستقوم بتحسين تصنيف لبنان في حال تضائلت إمكانيّة تعثّره عن سداد ديونه، وبأنّها ستخفّض هذا التصنيف في حال قامت الحكومة بالإعلان عن نيّتها بإعادة هيكلة الدين العام بالعملات المحليّة.