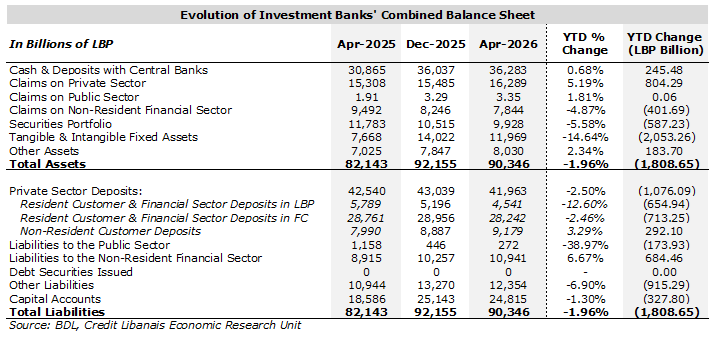

According to Banque Du Liban (BDL) statistics, the combined balance sheet of investment banks operating in Lebanon narrowed by 1.96% (LBP 1,808.65 billion) during the first four months of 2026 to LBP 90,346 billion, down from LBP 92,155 billion at end of 2025. In details, fixed assets dropped by 14.64% (LBP 2,053.26 billion) to LBP 11,969 billion and was accompanied by the 5.58% (LBP 587.23 billion) decrease in the value of the securities portfolio to LBP 9,928 billion, and the 4.87% (LBP 401.69 billion) drop in claims on the non-resident financial sector to LBP 7,844 billion, which altogether outweighed the 5.19% (804.29 billon) rise in claims on the private sector to LBP 16,289 billion, the 0.68% (LBP 245.48 billion) increase in cash and deposits with Central Banks to LBP 36,283 billion, and the 2.34% (LBP 183.70 billion) rise in the value of other assets to LBP 8,030 billion among others. On the liabilities side, investment banks’ private sector deposits decreased by 2.50% (LBP 1,076.09 billion) up until April 2026 to LBP 41,963 billion, coupled with the 6.90% (915.29 billion) drop in other liabilities to LBP 12,354 billion, and the 1.30% (LBP 327.80 billion) decrease in investment banks’ capital accounts to LBP 24,815 billion, have totally eroded the 6.67% (LBP 684.46 billion) rise in liabilities to the non-resident financial sector to LBP 10,941 billion,

Abiding by legislative decree number 50 and subsequent BDL circulars, investment banks operating in Lebanon have managed over the last couple of years to increase their lending activity to the private sector while reducing their exposure to the public sector. As a result, the surplus, representing the difference between loans to the private sector and claims on the public sector, reached LBP 16,286 billion in April 2026 compared to LBP 15,481 billion in December 2025 and LBP 15,306 billion in April 2025.

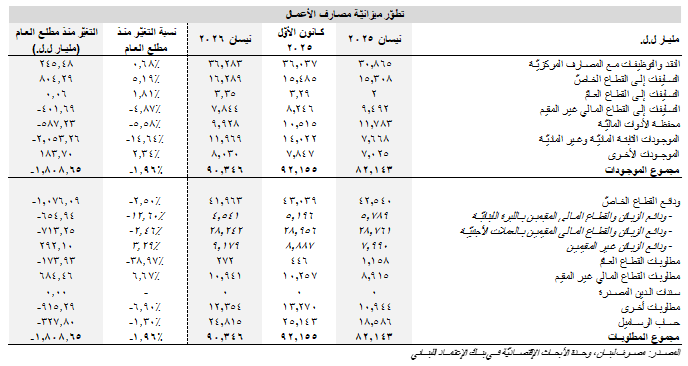

تُظهِر إحصاءات مصرف لبنان إنخفاضاً بنسبة 1.96% (1،808.65 مليار ل.ل.) في الموجودات المجمَّعة لمصارف الإستثمار العاملة في لبنان خلال الأشهر الأربعة الأولى من العام 2026 إلى 90،346 مليار ل.ل.، مقابِل 92،155 مليار ل.ل. في نهاية العام 2025. في التفاصيل، إنخفضت الموجودات الثابتة بنسبة 14.64% (2،053.26 مليار ل.ل.) إلى 11،969 مليار ل.ل.، رافقها تراجع في محفظة الأدوات الماليّة بنسبة 5.58% (587.23 مليار ل.ل.) إلى حوالي 9،928 مليار ل.ل. وتدنّي التسليفات إلى القطاع المالي غير المقيم بنسبة 4.87% (401.69 مليار ل.ل.) إلى 7،844 مليار ل.ل. للذكر لا الحصر، ما طغى على إرتفاع التسليفات إلى القطاع الخاصّ بنسبة 5.19% (804.29 مليار ل.ل.) إلى 16،289 مليار ل.ل. وزيادة رصيد النقد والتوظيفات مع المصارف المركزيّة بنسبة 0.68% (245.48 مليار ل.ل.) إلى 36،283 مليار ل.ل. وإرتفاع قيمة الموجودات الأخرى بنسبة 2.34% (183.70 مليار ل.ل.) إلى 8،030 مليار ل.ل. أمّا لجهة المطلوبات، فقد تراجعت ودائع القطاع الخاصّ لدى مصارف الإستثمار بنسبة 2.50% (1،076.09 مليار ل.ل.) حتّى شهر نيسان 2026 إلى 41،963 مليار ل.ل.، رافقها إنخفاض في قيمة المطلوبات الأخرى بنسبة 6.90% (915.29 مليار ل.ل.) إلى 12،354 مليار ل.ل. وتدنّي رصيد حساب الرساميل بنسبة 1.30% (327.80 مليار ل.ل.) إلى 24،815 مليار ل.ل.، ما طغى على الإرتفاع بنسبة 6.67% (684.46 مليار ل.ل.) في مطلوبات القطاع المالي غير المقيم لدى مصارف الإستثمار إلى 10،941 مليار ل.ل.

مراعاةً لتوصيات المصرف المركزي، نجحت مصارف الأعمال خلال السنوات القليلة المنصرمة بتعزيز محفظة تسليفاتها إلى القطاع الخاصّ مقابل توظيفاتها مع القطاع العامّ، مسجِّلةً فائضاً بقيمة 16،286 مليار ل.ل. مع نهاية شهر نيسان 2026 مقارنةً ب15،481 مليار ل.ل. في نهاية العام 2025 و15،306 مليار ل.ل. في نهاية شهر نيسان 2025.