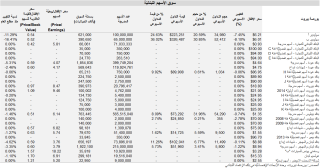

Activity on the Beirut Stock Exchange swirled deeper into the abyss despite the formation of a new government in the previous week. In fact, the number of shares changing hands plunged to 169,870 shares, compared to 293,712 shares last week, with traded value sinking to just below $0.91 million, from nearly $2.08 million a week before. Trades were mainly concentrated in real estate sector stocks, which accounted for 51.45% of weekly traded volume.

The average daily trading volume fell to 33,974 shares this week, from 58,742 shares in the previous week. Similarly, the average daily trading value narrowed to $0.18 million, from around $0.42 million a week earlier.

Seven losing and no gaining stocks were screened throughout the week, dragging the BSE’s market capitalization down by 1.26% week-on-week to about $9.29 billion and the Credit Libanais Aggregate Stock Index (“CLASI”) lower by 1.45% to a new year-low of 886.69.

In the real estate sector, trades solely consisted of Solidere “A” and “B” shares (51.45% of weekly traded volume), with the price of Solidere “A” dropping by 7.45% on a weekly basis to $6.21 and that of Solidere “B” shedding 8.10% to $6.01. Consequently, the Credit Libanais Construction Sector Stock Index (“CLCI”) ended its week 5.95% lower at 381.98.

In the banking sector, Byblos Bank listed shares amassed the highest concentration of trades (31.96% of total BSE traded volume) on a thin turnover ratio of 0.01%. The Credit Libanais Financial Sector Stock Index (“CLFI”) ended Friday’s session 0.47% lower week-on-week at 1,208.45. This comes as a result of the 0.74% weekly contraction in the price of Byblos Bank listed shares to $1.35, coupled with some 1.22% depreciation in the price of BLOM Bank listed shares to $8.94 and a 0.11% decrease in the price of BLOM Bank GDRs to $8.88.

The market-cap weighted average price to book value (P/BV) multiple of listed stocks ended its week lower at 0.651x based on the closing prices of Friday’s session.

تابعت حركة التداول على بورصة بيروت مسارها الإنحداري هذا الأسبوع بالرغم من تشكيل الحكومة الجديدة في الأسبوع الذي سبق. في التفاصيل، إنخفض عدد الأسهُم المتداوَلة على البورصة إلى 169،870 سهمٍ، مقابِل 293،712 سهمٍ في الأسبوع الفائت. كذلك تراجعت القيمة التداوليّة للأسهم إلى ما دون ال0.91 مليون د.أ.، مقارنةً بحوالي 2.08 مليون د.أ. في الأسبوع المنصرم. وقد سيطرت أسهُم القطاع العقاري على 51.45% من مجموع عدد الأسهُم المتداوَلة.

بالتوازي، إنكمش المتوسّط اليومي لعدد الأسهُم المتداوَلة إلى 33،974 سهمٍ هذا الأسبوع، من 58،742 سهمٍ في الأسبوع الذي سبقه، كما وتقلَّص متوسّط القيمة التداوليّة اليوميّة للأسهم إلى 0.18 مليون د.أ.، مقارنةً بنحو 0.42 مليون د.أ. في الأسبوع الماضي.

بالتوازي، إنخفضت الرسملة السوقيّة (Market Capitalization) لبورصة بيروت بنسبة 1.26% أسبوعيّاً إلى حوالي 9.29 مليار د.أ.، وذلك في ظلّ تدنّي سعر سبعة أسهُم وغياب أيّة أسهمٍ رابحة. في هذا السياق، أنهى مؤشّر بنك الإعتماد اللبناني للبورصة (“CLASI”) أسبوعه على إنكماشٍ بنسبة 1.45% ليصل إلى 886.69، وهو المستوى الأدنى له لهذا العام.

في القطاع العقاري، إقتصرت عمليّات التداول على أسهُم سوليدير "أ" و"ب" (51.45 % من مجموع عدد الأسهُم المتداوَلة)، مع تراجُع سعر سهم سوليدير "أ" بنسبة 7.45% على صعيدٍ أسبوعيٍّ إلى 6.21 د.أ. وتدنّي سعر سهم سوليدير "ب" بنسبة 8.10% إلى 6.01 د.أ. في هذا الإطار، إنخفض مؤشّر بنك الإعتماد اللبناني لأداء القطاع العقاري في البورصة (“CLCI”) بنسبة 5.95% على أساسٍ أسبوعيٍّ إلى 381.98.

أمّا في القطاع المصرفي، فقد إستحوذت الأسهُم العاديّة التابعة لبنك بيبلوس على حصّة الأسد (31.96%) من مجموع الأسهُم المتداوَلة خلال الأسبوع. من جهته، سَجَّلَ مؤشّر بنك الإعتماد اللبناني لأداء القطاع المالي في البورصة (“CLFI”) إنكماشاً أسبوعيّاً بنسبة 0.47% ليصل إلى 1،208.45. ويأتي ذلك نتيجة تراجُع سعر الأسهُم العاديّة التابعة لبنك بيبلوس بنسبة 0.74% إلى 1.35 د.أ.، ترافقاً مع إنخفاض سعر الأسهُم العاديّة التابعة لبنك لبنان والمهجر بنسبة 1.22% إلى 8.94 د.أ. وتدنّي سعر شهادات الإيداع التابعة لبنك لبنان والمهجر بنسبة 0.11% إلى 8.88 د.أ.

أنهى المتوسّط المثقَّل للسعر على القيمة الدفتريّة (P/BV) للأسهُم المدرَجة على بورصة بيروت أسبوعه على إنخفاضٍ ليستقرّ عند 0.651، بحسب أسعار إقفال نهار الجمعة.