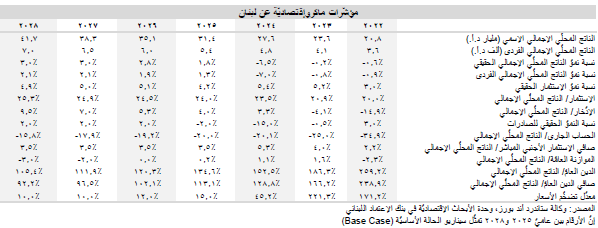

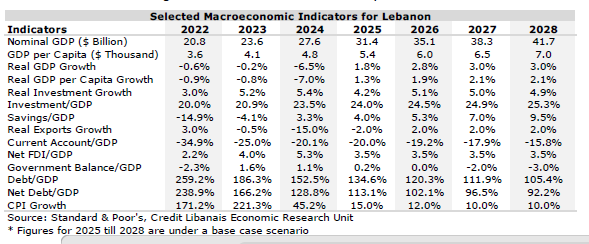

Standard & Poor’s Global Ratings (S&P), the international rating agency, improved on August 15, 2025 Lebanon’s long-term local currency rating by 3 notches to “CCC” from “CC” previously. In the meantime, the rating agency maintained the country’s long-term and short-term foreign currency (FC) ratings at “SD”, and the short-term local currency (LC) rating at “C”. The rating agency attributed the rating upgrade to the government's slightly better ability to manage its local debt, thanks to two consecutive years of budget surpluses and progress achieved on the reforms needed for a new IMF program. The rating agency cautioned, however, that the risk of a government default on domestic debt is still present due to ongoing spending pressures, limited access to financial markets and administrative and governance shortfalls. The rating agency also improved the outlook of Lebanon’s long-term LC rating to “Stable” from “Negative”, citing the balance between positive reform efforts and “significant” policy challenges such as weak economic growth, strained public finances, security concerns, and large-scale reconstruction needs. Always in the same regard, the rating agency stated that it does not expect local currency debt to be included in a government debt-restructuring plan under its base-case scenario expectations. S&P commented that it could lower the LC rating in the event of increased odds of the inclusion of local currency debt in a restructuring exercise, while ratings could further improve in the event additional progress is achieved on reforms that would eventually lead to better fiscal results, economic growth, and pave the way to concessional external funding. Always on the local currency debt front, S&P commented that the 98% depreciation of the Lebanese pound since the onset of the crisis in late 2019 has greatly reduced the value of LBP-denominated debt to below $1 billion (~2% of GDP and ~1% of gross government debt). The rating agency added that while the government remains current on its local currency payments to commercial banks (15% of total local currency debt), local currency payments to the Central Bank were halted between 2021 and 2023, yet were resumed in 2024 with plans from the government to repay the accumulated payments (2021 till 2023) starting the year 2025. The rating agency commended the country’s progress on reforms required for unlocking IMF funding, citing the parliament’s amendment of the banking secrecy law with a retroactive aspect of 10 years (to improve transparency on deposits) and the passing of the Bank Restructuring Law (which sets a legal & institutional framework for restructuring the banking sector). S&P noted, however, that the Financial Gap Law which will ultimately determine the nature, size and allocation of losses in the financial sector (and which serves as a pre-requisite for the implementation of the aforementioned Bank Restructuring Law) is yet to be passed. The rating agency also mentioned other reforms required to unlock external financing such as the adoption of a 2026 budget and medium-term fiscal plan, along with strengthening the Anti-Money Laundering and Combating the Financing of Terrorism legislation and reforming state-owned enterprises. Reforms execution risk remains elevated, however, according to the agency due to the limited time before the parliamentary elections in May 2026 and strained security situation with Israel. Standard & Poor’s added that barring the slight post-pandemic rebound in 2021, the country’s economy has been contracting in real terms since 2018, with real GDP shrinking by 6.5% in 2024 to $27.6 billion, down from around $55 billion in 2018. The rating agency commented, however, that this trend is expected to reverse starting the year 2025 as a gradual improvement in the security and political situation would pave the road to reform implementation and subsequently external financing that will facilitate reconstruction efforts. The rating agency added that the official exchange rate has been stable at the LBP 89,500/USD level since February 2024. S&P stated that the exchange rate stabilization coupled with the improved fiscal performance and increase in nominal GDP (due to inflation) have led to a massive drop in the net debt to GDP ratio to a projected 113% in 2025 from 239% in 2022. The rating agency expects government revenues to keep improving throughout the year 2028 due to better tax compliance efforts, yet anticipated expenditures to outpace revenues due to large reconstruction needs resulting in an average deficit to GDP ratio of 2.5% of GDP fiscal deficit over the 2027-2028 period. S&P projected the current account deficit to drop to an average of 18.2% over the 2025-2028 period, from 22.6% over the 2023-2024 period, yet commented that this figure remains elevated and can be financed by remittances and resident foreign currency savings. Finally, the rating agency pointed out that average annual inflation ebbed to 15% in H1-2025 down from 221% in 2023, while expecting the downward trend to be sustainable due to exchange rate stabilization and the high dollarization of the economy.

رفعت وكالة التصنيف الدوليّة ستاندرد أند بورز (S&P Global Ratings) في 15 آب 2025 تصنيف لبنان بالعملة المحليّة على المدى الطويل بثلاث درجات من "CC" إلى "CCC" في حين أبقت على التصنيف الطويل والقصير الأمد للديون السياديّة بالعملات الأجنبيّة عند التخلّف الإنتقائي عن الدفع "Selective Default" وتصنيف العملة المحليّة على المدى القصير عند "C". وعزت الوكالة رفع التصنيف إلى تحسّن قدرة الحكومة على إدارة دينها المحلّي بفضل الفوائض المحقّقة في الموازنة لعامين متتاليين والتقدّم المحرز في الإصلاحات المطلوبة من صندوق النقد الدولي. ومع ذلك، فقد حذّرت الوكالة من أنّ خطر تخلّف الحكومة عن سداد الدين المحلي لا يزال قائماً بسبب ضغوط الإنفاق المستمرّة ومحدوديّة الوصول إلى الأسواق الماليّة والقصور في مجاليّ الإدارة والحوكمة. كما حسّنت الوكالة النظرة المستقبليّة لتصنيف لبنان الائتماني الطويل الأجل بالعملة المحليّة من "سلبيّة" إلى "مستقرّة"، مشيرةً إلى التوازن بين جهود الإصلاح والتحدّيات الكبيرة كضعف النموّ الإقتصادي وضغط الماليّة العامّة والمخاوف الأمنيّة والإحتياجات الكبيرة لإعادة الإعمار. وفي السياق نفسه، ذكرت وكالة ستاندارد آند بورز بأنّها لا تتوقّع إدراج الدين بالعملة المحليّة في خطّة إعادة هيكلة الدين الحكومي في إطار سيناريو توقّعاتها المعتمد (Base Case Scenario). وعلّقت وكالة ستاندرد آند بورز بأنها قد تخفّض تصنيف الدين بالعملة المحليّة في حال زيادة احتمال إدراج الدين بالعملة المحليّة في عمليّة إعادة الهيكلة، في حين أنّها قد ترفع التصنيف أكثر في حال تحقيق تقدّم إضافي في الإصلاحات التي من شأنها أن تؤدي في نهاية المطاف إلى نتائج أفضل للماليّة العامّة ونموّ إقتصادي وفتح الباب أمام تمويل خارجي بشروط ميسّرة. وقد علّقت الوكالة بأنّ إنخفاض سعر صرف الليرة اللبنانيّة مقابل الدولار الأميركي بنسبة 98% قد أدّى إلى تراجع كبير في قيمة الدين المقوّم بالليرة اللبنانيّة إلى أقلّ من مليار د.أ. (حوالي 2% من الناتج المحلّي الإجمالي وحوالي 1% من إجمالي الدين الحكومي). وأضافت وكالة التصنيف الائتماني أنه في حين أنّ الحكومة بقيت ملتزمة بسداد مستحقاتها بالعملة المحليّة للمصارف (15% من إجمالي الدين بالعملة المحليّة)، فإنّها توقّفت عن دفع مستحقّاتها بالليرة اللبنانيّة للبنك المركزي بين عاميّ 2021 و2023، إلا أنّها إستأنفت هذه الدفعات في العام 2024، كما وأنّها تخططّ لسداد الدفعات المتراكمة (من 2021 إلى 2023) بدءاً من العام 2025. وأشادت وكالة التصنيف الائتماني بالتقدّم الذي أحرزته البلاد في الإصلاحات اللازمة للحصول على تمويل من قبل صندوق النقد الدولي، مشيرةً في هذا السياق إلى تعديل البرلمان لقانون السريّة المصرفيّة بمفعول رجعي لمدّة 10 سنوات (لتحسين الشفافية بشأن الودائع)، وإقرار قانون إعادة هيكلة المصارف (الذي يضع إطاراً قانونيّاً ومؤسّسياً لإعادة هيكلة القطاع المصرفي). ومع ذلك، أشارت الوكالة إلى أنّ قانون الفجوة الماليّة الذي سيحدّد في نهاية المطاف طبيعة وحجم وتوزيع الخسائر في القطاع المالي (والذي يُعد شرطاً أساسياً لتطبيق قانون إعادة هيكلة المصارف المذكور أعلاه)، لم يُقرّ بعد. كما أشارت وكالة التصنيف الائتماني إلى إصلاحات أخرى مطلوبة لتسهيل التمويل الخارجي، مثل إقرار موازنة العام 2026 وخطة ماليّة متوسّطة الأجل، إلى جانب تعزيز تشريعات مكافحة غسل الأموال وتمويل الإرهاب وإصلاح الشركات المملوكة من الدولة. ومع ذلك، لا تزال مخاطر التنفيذ مرتفعةً وفقاً للوكالة، نظراً لضيق الوقت قبل الإنتخابات البرلمانيّة في أيّار 2026 والوضع الأمني المتوتر مع إسرائيل. وأضافت وكالة ستاندرد آند بورز أنّه بإستثناء الإنتعاش الطفيف المسجّل بعد جائحة كورونا في العام 2021، فإن إقتصاد البلاد قد إستمّر بالتراجع منذ العام 2018، مع إنكماش الناتج المحلّي الإجمالي الحقيقي بنسبة 6.5٪ في العام 2024 إلى 27.6 مليار د.أ. مقارنةً مع حوالي 55 مليار د.أ. في العام 2018. ومع ذلك، علّقت وكالة التصنيف بأنّه من المتوقّع بأن ينعكس هذا النمط بدءاً من العام 2025، حيث أنّ التحسّن التدريجي في الوضعين الأمني والسياسي من شأنه أن يمهّد الطريق لتنفيذ الإصلاحات، وبالتالي فتح الباب للتمويل الخارجي الذي سيسهّل جهود إعادة الإعمار. وأضافت وكالة التصنيف بأنّ سعر الصرف الرسمي قد بقي مستقراً عند مستوى 89،500 ليرة لبنانيّة مقابل الدولار الأميركي منذ شهر شباط 2024 وهو ما ساعد إلى جانب تحسّن الأداء المالي وزيادة الناتج المحلّي الإجمالي الاسمي (بسبب التضخّم) بإنخفاض كبير متوقّع في نسبة صافي الدين إلى الناتج المحلي الإجمالي إلى 113٪ في العام 2025 من 239٪ في العام 2022. وتوقّعت وكالة التصنيف بأن تستمرّ الإيرادات الحكوميّة في التحسّن لغاية العام 2028 بسبب تحسّن جهود الإمتثال الضريبي، إلا أنها إرتقبت بأن تتجاوز النفقات الحكوميّة الإيرادات المتوقّعة بسبب إحتياجات إعادة الإعمار الكبيرة مما سيؤدي إلى متوسّط عجز في الموازنة العامة عند 2.5٪ من الناتج المحلّي الإجمالي خلال عاميّ 2027 و2028. وتوقّعت وكالة ستاندرد آند بورز بأن ينخفض متوسّط العجز في الحساب الجاري إلى 18.2٪ من الناتج المحلّي الإجمالي خلال الفترة الممتدّة بين عاميّ 2025 و2028، من 22.6٪ خلال الفترة الممتدّة بين عاميّ 2023 و2024، إلا أنّها علّقت بأنّ هذا العجز لا يزال مرتفعاً وسيتم تمويله من تحويلات المغتربين الوافدة إلى لبنان ومن ودائع المقيمين بالعملة الأجنبيّة. وأخيراً، أشارت وكالة التصنيف الائتماني إلى أن متوسّط التضخّم السنوي قد إنخفض إلى 15% في النصف الأول من العام 2025 من 221% في عام 2023، كما وتوقّعت بأن يستمر هذا النمط بسبب إستقرار سعر الصرف والدولرة المرتفعة للإقتصاد.