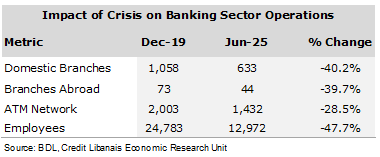

Banque Du Liban’s recent Macroeconomic Review publication which covers the first half of 2025 shed light on the current situation of the banking sector pointing out that the sector currently comprises 57 banks, of which 45 commercial (36 Lebanese-owned down from 38 at the start of the crisis and 9 foreign-owned) and 12 investment banks (down from 16 pre-crisis). The review added that banks were compelled into downsizing their operations as a result of the crisis, whether in terms of domestic branches which were reduced by 425 (40.2%) to 633, number of branches abroad which shrank by 29 (39.7%) to 44, ATM network which contracted by 571 machines (28.5%) to 1,432 or taskforce which fell by 11,811 employees (47.7%) to 12,972. This is further outlined by the below table:

The crisis also had a profound impact on major elements of commercial banks’ balance sheet as highlighted by the below section:

- Sovereign Placements and Placements with BDL: The securities portfolio fell from $34.8 billion in June 2019 to $7.0 billion six years later mainly on the back of the contraction of the value of the Eurobonds portfolio coupled with the steep depreciation of the local currency that reduced the dollar value of LBP-denominated treasury bills from $16.8 billion to ~$94 million. Moreover, banks’ deposits at BDL declined sharply from $143.8 billion to $79.2 billion.

- Loans: The massive loan repayments witnessed during the crisis coupled with the depreciation of the local currency led to a sharp contraction in the size of the loan portfolio at commercial banks. In details, the size of the portfolio fell from $56 billion in June 2019 ($39.2 billion in foreign currency “FC” loans and $16.8 billion in local currency “LC” loans) to $5.5 billion in June 2025 ($5.3 billion in FC loans and $132 million in LC loans). BDL commented that as a result of the exchange rate divergence, the real value of loan repayments is “substantially” lower than their nominal value and accordingly “sizable” losses were incurred by banks. As far as fresh lending activity is concerned, the Central Bank commented that it remains minimal, with the value of fresh dollar loans reaching $553 million by June 2025 compared to $358 million at end of November 2023. The review added that these fresh loans are mainly in the form of small personal loans charging “extremely high” interest rates and requiring stringent eligibility criteria (such as salary domiciliation) that exclude large segments of the population and businesses. The Central Bank expects that barring a comprehensive restructuring of the banking sector and a resolution for depositors, lending activity is expected to remain timid with banks preferring self-preservation over economic support.

- Asset Quality: BDL commented that the banking sector experienced a significant deterioration in loan quality due to the financial crisis and currency depreciation. Non-performing loans (NPLs) rose sharply across all loan categories, mainly amplified by a "denominator effect". Accordingly, the ratio of NPLs rose significantly across several loan size tranches, ranging from 78.4% for loans under LBP 10 billion to 86.8% for loans above LBP 50 billion as of February 2025.

- Deposits: The size of the deposit portfolio fell from $172.1 billion in June 2019 ($123.1 billion in FC deposits and $49.1 billion in LC deposits) to $88.8 billion in June 2025 ($87.3 billion in FC deposits and $0.9 billion in LC deposits). BDL commented that LBP deposits were mainly exhausted by withdrawals and the devaluation of the local currency while foreign currency deposits were mainly used for loan settlement. As far as fresh deposits are concerned, the review revealed that the size of fresh deposits has attained $4.36 billion as at end of June 2025, of which $2.2 billion constitute outstanding balances under BDL circular 158 accounts and thus do not represent actual liquidity since they are subject to gradual repayment. As for the remaining $2.16 billion, these represent fresh deposits that must be fully provisioned for by banks (minimum liquidity threshold of 100%) by holding equivalent balances in their branches or with correspondent banks abroad, and consequently have no multiplier effect and can’t be used to support “lending, investment or broader financial intermediation”.

- Equity: Capital accounts at commercial banks fell from $20.9 billion in June 2019 to $5.2 billion in June 2025 amid the recurrent losses registered by banks. BDL commented in this regard that the current capitalization level at banks reduces their ability to absorb shocks.

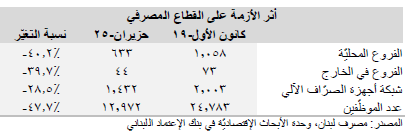

ألقت النشرة الأولى من المراجعة الكليّة الإقتصاديّة التي أصدرها مصرف لبنان مؤخّراً عن النصف الأول من العام 2025 الضوء على الوضع الحالي للقطاع المصرفي. وأشار التقرير أولاً إلى أنّ القطاع المصرفي اللبناني يضم 57 مصرفاً، منها 45 مصرفاً تجاريّاً (36 مصرفاّ مملوكاً من لبنانيين بإنخفاض عن 38 في بداية الأزمة و9 مصارف مملوكة من أجانب) و12 مصرف إستثمار (بانخفاض عن 16 قبل الأزمة). وأضاف التقرير بأنّ المصارف قد إضطرّت إلى تقليص عمليّاتها نتيجة الأزمة، سواء من حيث عدد الفروع المحليّة التي إنخفضت بمقدار 425 فرعاً (40.2%) إلى 633 فرعاً أو عدد الفروع في الخارج التي تقلّصت بمقدار 29 فرعاً (39.7%) إلى 44 فرعاً أو شبكة أجهزة الصرّاف الآلي التي تراجعت بمقدار 571 جهازاً (28.5٪) إلى 1،432 أو اليد العاملة التي إنخفضت بمقدار 11،811 موظّفاً (47.7٪) إلى 12،972 كما هو موضح في الجدول أدناه:

وقد كان للأزمة أيضاً أثر بالغ على العناصر الرئيسيّة في ميزانيّة المصارف التجاريّة، كما هو موضح في القسم التالي:

- التوظيفات السياديّة وتلك لدى مصرف لبنان: إنخفضت محفظة الأوراق الماليّة من 34.8 مليار د.أ. في شهر حزيران 2019 إلى 7.0 مليارات د.أ. بعد ست سنوات، وهو ما يمكن عزوه إلى إنكماش قيمة محفظة سندات اليوروبوند إلى جانب تدهور سعر صرف العملة المحليّة الذي قلّص قيمة سندات الخزينة المقوّمة بالليرة اللبنانيّة من 16.8 مليار د.أ. إلى حوالي 94 مليون د.أ. علاوةً على ذلك، فقد إنخفضت ودائع المصارف لدى مصرف لبنان بشكلٍ حاد من 143.8 مليار د.أ. إلى 79.2 مليار د.أ.

- محفظة القروض: أدّت عمليات السداد الضخمة للقروض التي شهدتها المصارف التجاريّة خلال الأزمة بالإضافة إلى التدهور الحاد في سعر صرف العملة المحليّة إلى إنكماش كبير في حجم محفظة التسليفات الذي تراجع من 56 مليار د.أ. في حزيران 2019 (39.2 مليار د.أ. منها قروض بالعملة الأجنبيّة و16.8 مليار د.أ. قروض بالعملة المحليّة) إلى 5.5 مليار د.أ. في حزيران 2025 (5.3 مليار د.أ. منها قروض بالعملة الأجنبيّة و132 مليون د.أ. قروض بالعملة المحليّة). وعلّق مصرف لبنان قائلاً بأنّه نتيجةً للتباين في سعر الصرف فقد كانت القيمة الحقيقيّة للقروض المسدّدة أقل بكثير من قيمتها الدفتريّة وهو ما كبّد المصارف خسائر كبيرة. أمّا فيما يتعلق بالقروض الفريش فقد أشار المصرف المركزي إلى أنّها لا تزال في مستويات منخفضة حيث بلغت قيمة تلك القروض 553 مليون د.أ. بحلول شهر حزيران 2025 مقارنةً بـ 358 مليون د.أ. في نهاية تشرين الثاني 2023. وأضاف التقرير بأنّ هذه القروض تأتي في الغالب على شكل قروض شخصيّة صغيرة بأسعار فائدة مرتفعة للغاية كما وتفرض معايير أهليّة صارمة مثل توطين الراتب، ممّا يستبعد شرائح كبيرة من السكّان والشركات. ويتوقّع المصرف المركزي بأنّه من المتوقّع بأنّ يظل نشاط الإقراض خجولاً ما لم تتم إعادة هيكلة شاملة للقطاع المصرفي وحلّ لمشكلة المودعين.

- جودة الأصول: أشار مصرف لبنان إلى أنّ القطاع المصرفي قد شهد تدهوراً كبيراً في جودة القروض بسبب الأزمة الماليّة وتدهور سعر صرف العملة. بالتفاصيل، فقد إرتفعت نسبة القروض المتعثّرة بشكل حاد، وهو ما يعزى بشكل رئيسي إلى تأثير القاسم المشترك (Denominator Effect). وبناءً على ذلك، إرتفعت نسبة القروض المتعثرة بشكل ملحوظ عبر مختلف شرائح أحجام القروض، حيث تراوحت بين 78.4% للقروض التي تقلّ عن 10 مليارات ل.ل. و86.8% للقروض التي تزيد عن 50 مليار ل.ل. إعتباراً من شهر شباط 2025.

- الودائع: تراجع حجم محفظة الودائع من 172.1 مليار د.أ. في حزيران 2019 (123.1 مليار د.أ. منها ودائع بالعملات الأجنبيّة و49.1 مليار د.أ. ودائع بالعملة المحليّة) إلى 88.8 مليار د.أ. في حزيران 2025 (87.3 مليار د.أ. منها ودائع بالعملات الأجنبيّة و0.9 مليار د.أ. ودائع بالعملة المحليّة). وعلّق مصرف لبنان بأنّ الودائع بالليرة اللبنانيّة قد إستُنفذت بشكل رئيسي بسبب عمليات السحب وتراجع سعر صرف العملة المحليّة، بينما إستُخدمت الودائع بالعملات الأجنبيّة بشكل رئيسي لتسوية القروض. فيما يتعلق بالودائع الفريش، كشف مصرف لبنان بأنّ حجمها قد بلغ 4.36 مليار د.أ. بنهاية حزيران 2025، منها 2.2 مليار د.أ. أرصدة قائمة بموجب تعميم مصرف لبنان رقم 158، وبالتالي لا تُمثل سيولة فعليّة لأنها تخضع للسداد التدريجي. أما المبلغ المتبقي، وقدره 2.16 مليار د.أ.، فهو يُمثّل ودائع جديدة يتعين على المصارف تحويطها بالكامل (بحد أدنى للسيولة بنسبة 100%) من خلال الإحتفاظ بأرصدة معادلة في فروعها أو لدى بنوك مراسلة في الخارج، وبالتالي ليس لها تأثير مضاعف، ولا يمكن إستخدامها لدعم الإقراض أو الإستثمار أو الوساطة الماليّة.

- حقوق الملكية: إنخفضت حسابات رأس المال لدى المصارف التجارية من 20.9 مليار د.أ. في حزيران 2019 إلى 5.2 مليار د.أ. في حزيران 2025، في ظلّ الخسائر المتكرّرة التي تُسجّلها المصارف. وعلّق مصرف لبنان في هذا الصدد بأنّ مستوى الرسملة الحالي لدى المصارف يُقلل من قدرتها على إمتصاص الصدمات.