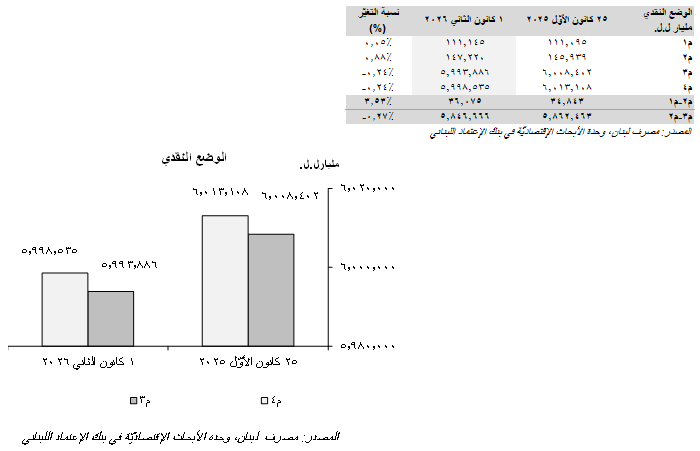

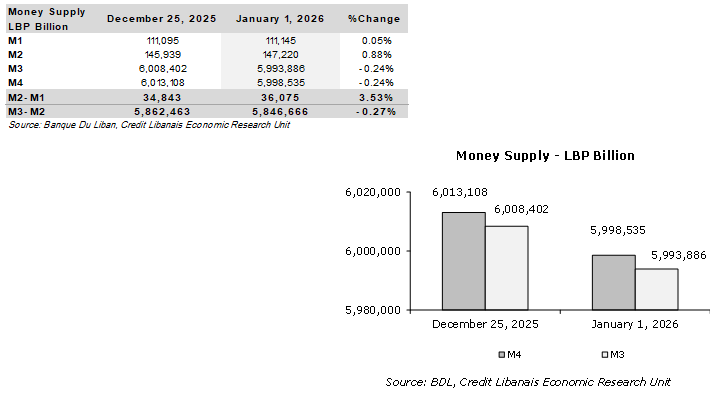

The overall money supply, “M4”, narrowed by LBP 14,572.95 billion during the week of January 1 to LBP 5,998.54 trillion, noting that the non-banking sector’s Treasury bills portfolio decreased by LBP 57.04 billion during the concerned week.

In parallel, Lebanese-Pound denominated deposits and currency in circulation, “M1”, rose by LBP 50.06 billion week-on-week to LBP 111,145 billion on the back of the LBP 1,029.57 billion increase in currency in circulation which outweighed the LBP 979.51 billion decrease in demand deposits. Local currency term deposits, “M2”, increased by LBP 1,281.60 billion on a weekly basis to settle at LBP 147,220 billion.

Consequently, private sector term and saving deposits denominated in LBP (“M2-M1”) widened by LBP 1,231.53 billion (3.53%) to LBP 36,075 billion during the week of January 1, while deposits denominated in foreign currencies (“M3-M2”) sank by LBP 15,797.50 billion (0.27%) to LBP 5,846.67 trillion.

إنخفضت الكتلة النقديّة بمفهومها الواسع، "م4"، ب14،572.95 مليار ل.ل. خلال الأسبوع المنتهي في 1 كانون الثاني إلى 5،998.54 ترليون ل.ل. علماً أنّ محفظة سندات الخزينة المكتتَب بها من قِبَل القطاع غير المصرفي قد إنخفضت ب57.04 مليار ل.ل. في الأسبوع المذكور.

في المقابل، إرتفعت الكتلة النقديّة "م1"، والتي تشمل السيولة الجاهزة بالليرة اللبنانيّة، ب50.06 مليار ل.ل. على أساسٍ أسبوعيٍّ إلى 111،145 مليار ل.ل.، وذلك بفعل زيادة حجم النقد المتداول ب1،029.57 مليار ل.ل. ما طغى على إنخفاض حجم الودائع تحت الطلب ب979.51 مليار ل.ل. وقد زادت الكتلة النقديّة بالليرة اللبنانيّة، "م2"، ب1،281.60 مليار ل.ل. لتصل إلى 147،220 مليار ل.ل.

في هذا الإطار، إرتفع حجم الإدّخار بالعملة الوطنيّة (م2-م1) ب1،231.53 مليار ل.ل. (3.53%) إلى 36،075 مليار ل.ل. في الأسبوع المنتهي في 1 كانون الثاني فيما تراجع رصيد الودائع المعنونة بالعملات الأجنبيّة (م3-م2) ب15،797.50 مليار ل.ل. (0.27%) إلى 5،846.67 ترليون ل.ل.