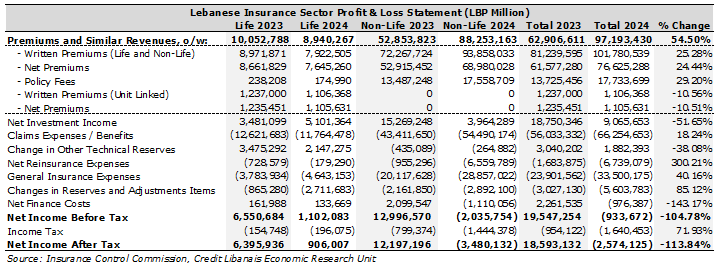

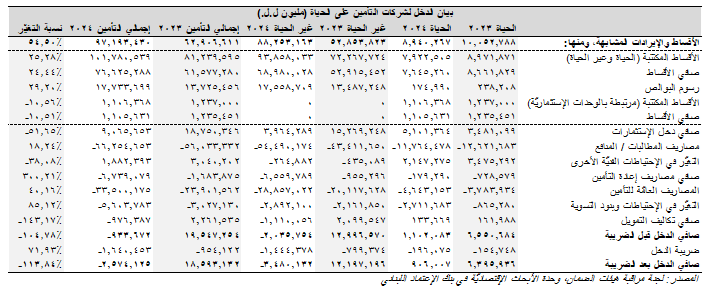

The Insurance Control Commission published its 2024 Annual Report conveying a net loss of LBP 2.57 trillion in 2024, compared to a net income of LBP 18.59 trillion in 2023. In details, the sector recorded a sizeable increase (54.50%) in premiums & similar revenues to LBP 97.19 trillion in 2024, compared to LBP 62.91 trillion in 2023. This increase can be mainly attributed to the 24.44% rise in net written premiums in life and no-life insurance to LBP 76.63 trillion, coupled with some 29.20% hike in policy fees to LBP 17.73 trillion. On the other hand, insurance companies recorded a 51.65% drop in net investment income to LBP 9.07 trillion in 2024 down from LBP 18.75 trillion in 2023. In parallel, the sector saw a sharper increase in operating expenses compared to its revenues. More specifically, claims expenses rose by 18.24% in 2024 to LBP 66.25 trillion, with net reinsurance expenses skyrocketing by 300.21% to LBP 6.74 trillion, and general insurance expenses soaring by 40.16% to LBP 33.50 trillion, among others.

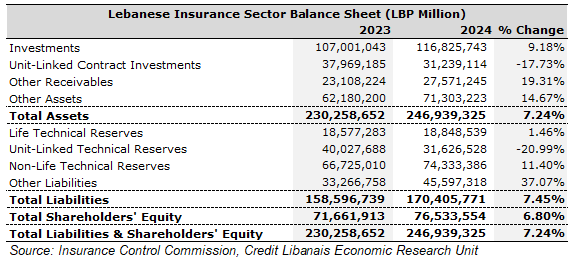

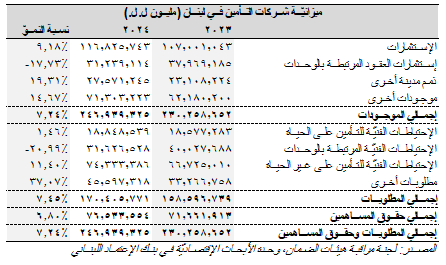

On the balance sheet front, the Lebanese insurance sector’s total assets saw a 7.24% increase in 2024 to just below LBP 246.94 trillion, up from LBP 230.26 trillion in 2023 mainly buoyed by the 9.18% rise in investments to LBP 116.83 trillion, and the 19.31% increase in other receivables to LBP 27.57 trillion, among others. On the liabilities and shareholders’ equity front, the Lebanese insurance sector’s total liabilities rose by 7.45% in 2024 to LBP 170.41 trillion mainly owing to the 11.40% increase in non-life technical reserves to LBP 74.33 trillion, noting that shareholders’ equity rose by 6.80% to LBP 76.53 trillion.

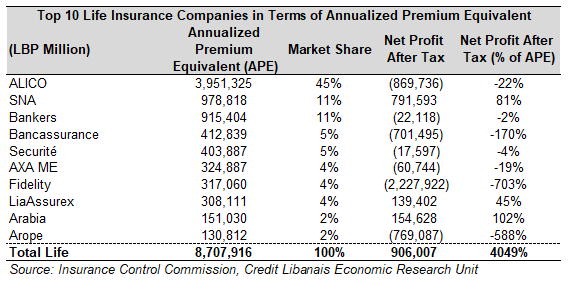

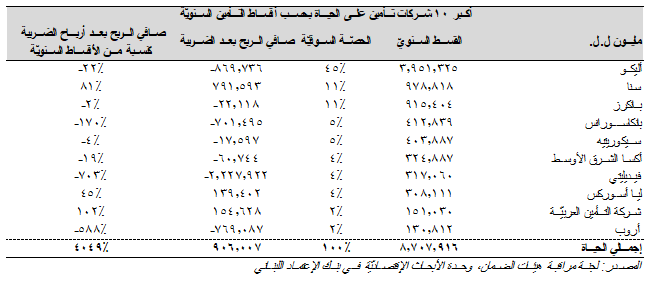

Concerning life insurance companies, the ICC revealed that ALICO emerged as the company with the largest Annualized Premium Equivalent (APE) in 2024, with its’ APE reaching LBP 3.95 trillion and representing a 45% market share of total life insurance companies’ APE (net after-tax loss of LBP 0.87 trillion). ALICO was followed by SNA (APE of LBP 0.98 trillion, market share of around 11%, net after-tax profit of LBP 0.79 trillion), and Bankers (APE of LBP 0.92 trillion, market share of around 11%, net after-tax loss of LBP 0.02 trillion), only to name a few.

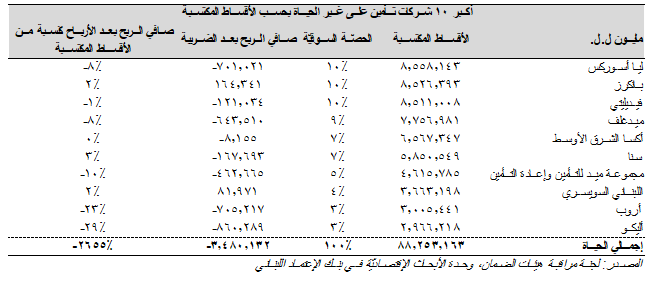

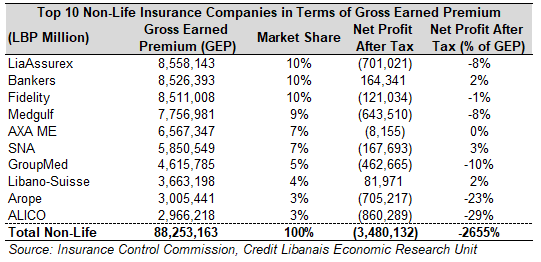

As for non-life insurance companies, LiaAssurex amassed the largest Gross Earned Premium (GEP) among Lebanese insurance companies in 2024, with its’ GEP totaling LBP 8.56 trillion (~10% market share and a net after-tax loss of LBP 0.70 trillion). Bankers came in second on the list (GEP of LBP 8.53 trillion, market share of circa 10%, and a net after-tax profit of around LBP 0.16 trillion), and Fidelity (GEP of LBP 8.51 trillion, market share of around 10%, and a net after-tax loss of LBP 0.12 trillion, among others.

أصدَرَت لجنة مراقبة هيئات الضمان تقريرها السنويّ عن العام 2024 كشفت من خلاله عن خسائر صافية بقيمة 2.57 ترليون ل.ل. خلال العام 2024 مقارنةً بأرباح صافية بلغت 18.59 ترليون ل.ل. خلال العام 2023. بالتفاصيل، فقد سجّل قطاع التأمين إرتفاعاً ملحوظاً في الأقساط والإيرادات المشابهة بنسبة 54.50% لتصل إلى 97.19 ترليون ل.ل. في العام 2024 مقارنةً ب62.91 ترليون ل.ل. في العام 2023. يمكن تعليل هذا الإرتفاع بزيادة صافي الأقساط المكتتبة على تأمينات الحياة وغير الحياة بنسبة 24.44% إلى 76.63 ترليون ل.ل. وإرتفاع رسوم البوالص بنسبة 29.20% إلى 17.73 ترليون ل.ل. من ناحية أخرى، سجّلت شركات التأمين تراجع في صافي دخل الإستثمارات بنسبة 51.65% إلى 9.07 ترليون ل.ل. في العام 2024 من 18.75 ترليون ل.ل. في العام 2023. في المقابل، زادت المصاريف التشغيليّة بنسب فاقت الزيادة في الإيرادات. بالتفاصيل، إرتفعت مصاريف المطالبات بنسبة 18.24% في العام 2024 إلى 66.25 ترليون ل.ل. كما وزادت كلفة صافي إعادة التأمين بشكلٍ مضطرد (300.21%) إلى 6.74 ترليون ل.ل. وإرتفعت المصاريف العامّة للتأمين بنسبة 40.16% إلى 33.50 ترليون ل.ل. للذكر لا الحصر.

أمّا لجهة ميزانيّة شركات التأمين، فقد شهدت موجوداتها إرتفاعاً بنسبة 7.24% في العام 2024 إلى ما دون ال246.94 ترليون ل.ل. من 230.26 ترليون ل.ل. في العام 2023 نتيجة إرتفاع حجم الإستثمارات بنسبة 9.18% إلى 116.83 ترليون ل.ل. وزيادة الذمم المدينة الأخرى بنسبة 19.31% إلى 27.57 ترليون ل.ل. أمّا على صعيد المطلوبات وحقوق المساهمين، فقد زاد إجمالي مطلوبات قطاع التأمين بنسبة 7.45% في العام 2024 إلى 170.41 ترليون ل.ل. بسبب إرتفاع حجم الإحتياطات الفنيّة للتأمين على غير الحياة بنسبة 11.40% إلى 74.33 ترليون ل.ل.، مع العلم أنّ الأموال الخاصّة قد زادت أيضاً بنسبة 6.80% إلى 76.53 ترليون ل.ل.

أمّا لناحية شركات التأمين على الحياة، فقد كشف تقرير لجنة مراقبة هيئات الضمان أنّ شركة أليكو قد حظيت على أعلى أقساط التأمين السنويّة والتي بلغت 3.95 ترليون ل.ل. في العام 2024 أيّ حصّة 45% في السوق (خسائر صافية بعد الضريبة بقيمة 0.87 ترليون ل.ل.)، تبعتها شركة سنا (أقساط سنويّة: 0.98 ترليون ل.ل.، حصّة سوقيّة: حوالي 11%، أرباح صافية بعد الضريبة 0.79 ترليون ل.ل.) وشركة بانكرز (أقساط سنويّة: 0.92 ترليون ل.ل.، حصّة سوقيّة: حوالي 11%، خسائر صافية بعد الضريبة: 0.02 ترليون ل.ل.) للذكر لا الحصر.

أمّا لجهة شركات التأمين على غير الحياة، فقد حصلت شركة ليا أسوريكس على أكبر أقساط مكتسبة ضمن شركات التأمين اللبنانيّة في العام 2024 حيث بلغت 8.56 ترليون ل.ل. (حصّة سوقيّة: حوالي 10%، خسائر صافية بعد الضريبة: 0.70 ترليون ل.ل.)، متبوعةً من شركة بانكرز (أقساط مكتسبة: 8.53 ترليون ل.ل.، حصّة سوقيّة: حوالي 10%، أرباح صافية بعد الضريبة: 0.16 ترليون ل.ل.) وشركة فيديليتي (أقساط مكتسبة: 8.51 ترليون ل.ل.، حصّة سوقيّة: حوالي 10%، خسائر صافية بعد الضريبة: 0.12 ترليون ل.ل.) وغيرها.